Attorney-Approved Texas Loan Agreement Document

Attorney-Approved Texas Loan Agreement Document

Understanding the Texas Loan Agreement form is crucial for anyone involved in borrowing or lending money in Texas. However, several misconceptions can lead to confusion. Here are eight common misconceptions about this form, along with clarifications.

Being aware of these misconceptions can help you navigate the loan process more effectively and protect your interests. Always consider consulting a legal professional for personalized advice and guidance.

Completing the Texas Loan Agreement form is an important step in securing a loan. This process requires careful attention to detail to ensure that all necessary information is accurately provided. Follow these steps to fill out the form correctly.

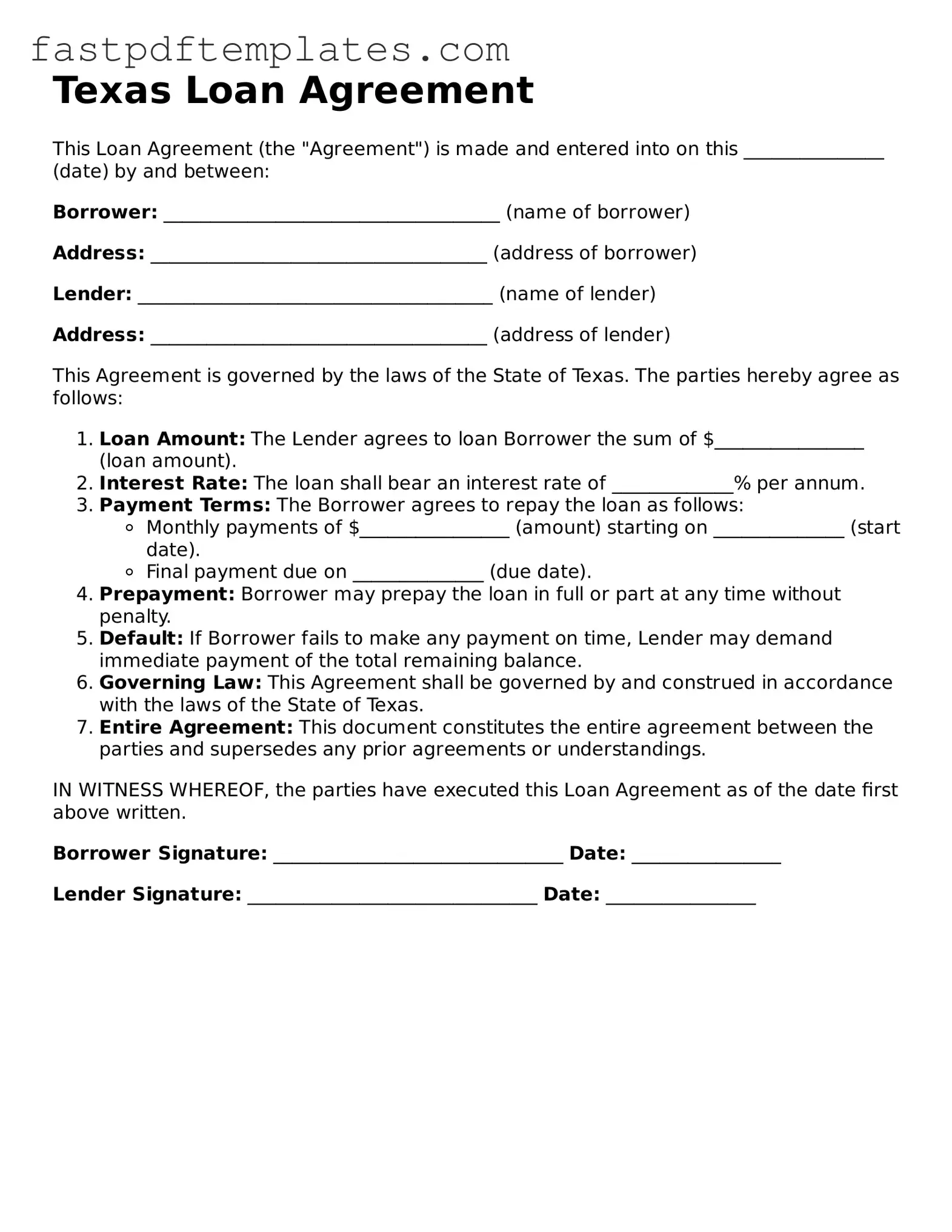

Texas Loan Agreement

This Loan Agreement (the "Agreement") is made and entered into on this _______________ (date) by and between:

Borrower: ____________________________________ (name of borrower)

Address: ____________________________________ (address of borrower)

Lender: ______________________________________ (name of lender)

Address: ____________________________________ (address of lender)

This Agreement is governed by the laws of the State of Texas. The parties hereby agree as follows:

IN WITNESS WHEREOF, the parties have executed this Loan Agreement as of the date first above written.

Borrower Signature: _______________________________ Date: ________________

Lender Signature: _______________________________ Date: ________________

Loan Agreement Template California - This form specifies the amount borrowed and the repayment schedule.

Promissory Note Illinois - The agreement may outline procedures for handling loan payoff statements.

Promissory Note New York - This document may detail borrower eligibility requirements.

Loan Note Template - A Loan Agreement outlines the terms between a lender and a borrower.

When filling out the Texas Loan Agreement form, it's important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn't do:

When filling out and using the Texas Loan Agreement form, it is essential to understand several key points to ensure compliance and clarity. Below are the critical takeaways to consider:

By adhering to these takeaways, individuals can navigate the Texas Loan Agreement process more effectively and reduce the risk of misunderstandings.

The Texas Promissory Note is a document that outlines the borrower's promise to repay a specific amount of money to the lender. Like the Loan Agreement form, it includes essential details such as the loan amount, interest rate, and repayment terms. However, the Promissory Note focuses primarily on the borrower's commitment, while the Loan Agreement may also cover additional terms and conditions related to the loan, such as collateral requirements and default consequences. Both documents serve to protect the interests of the lender and establish clear expectations for the borrower.

The Texas Security Agreement is another document that shares similarities with the Loan Agreement form. This document is used when a borrower pledges collateral to secure a loan. Like the Loan Agreement, it outlines the terms of the loan and the obligations of both parties. However, the Security Agreement specifically details the collateral being offered and the lender's rights in the event of default. Together, these documents provide a comprehensive understanding of the loan and its security provisions.

The Texas Mortgage Agreement is a document that is often associated with real estate transactions. It serves as a legal contract between a borrower and a lender, detailing the terms of a loan used to purchase property. Similar to the Loan Agreement, it includes information about the loan amount, interest rate, and repayment schedule. The Mortgage Agreement, however, specifically ties the loan to the property being purchased, granting the lender a lien on the property until the loan is repaid. This adds an additional layer of security for the lender compared to a standard Loan Agreement.

The Texas Lease Agreement also bears similarities to the Loan Agreement form in that it establishes a contractual relationship between two parties. While a Lease Agreement pertains to the rental of property, it includes terms such as payment amounts, duration, and responsibilities of both the landlord and tenant. Like the Loan Agreement, it aims to protect the interests of both parties by clearly outlining expectations and obligations. However, the Lease Agreement is focused on rental arrangements rather than loans, making it a different type of financial agreement.

The Texas Installment Sale Agreement is another document that can be compared to the Loan Agreement. This agreement allows a buyer to purchase an item, such as a vehicle or equipment, through a series of installment payments. Similar to a Loan Agreement, it outlines the purchase price, payment schedule, and interest rate. However, the Installment Sale Agreement typically includes provisions regarding ownership transfer, which occurs once all payments have been made. This distinguishes it from a standard Loan Agreement, where ownership of the loaned item may not transfer until the loan is fully repaid.

When entering into a loan agreement in Texas, several additional forms and documents may be necessary to ensure clarity and legal compliance. These documents help outline the terms of the loan, protect the interests of both parties, and provide a clear framework for the transaction.

Understanding these documents can help you navigate the loan process more effectively. Each plays a vital role in protecting both the lender and the borrower, ensuring that all parties are aware of their rights and responsibilities.