Attorney-Approved Texas Deed in Lieu of Foreclosure Document

Attorney-Approved Texas Deed in Lieu of Foreclosure Document

Understanding the Texas Deed in Lieu of Foreclosure form is crucial for homeowners facing financial difficulties. However, several misconceptions can lead to confusion. Here are four common misunderstandings:

Once you have the Texas Deed in Lieu of Foreclosure form ready, you will need to carefully fill it out to ensure all necessary information is included. After completing the form, you will typically submit it to the lender for approval. This process can help facilitate a smoother transition out of homeownership.

Texas Deed in Lieu of Foreclosure

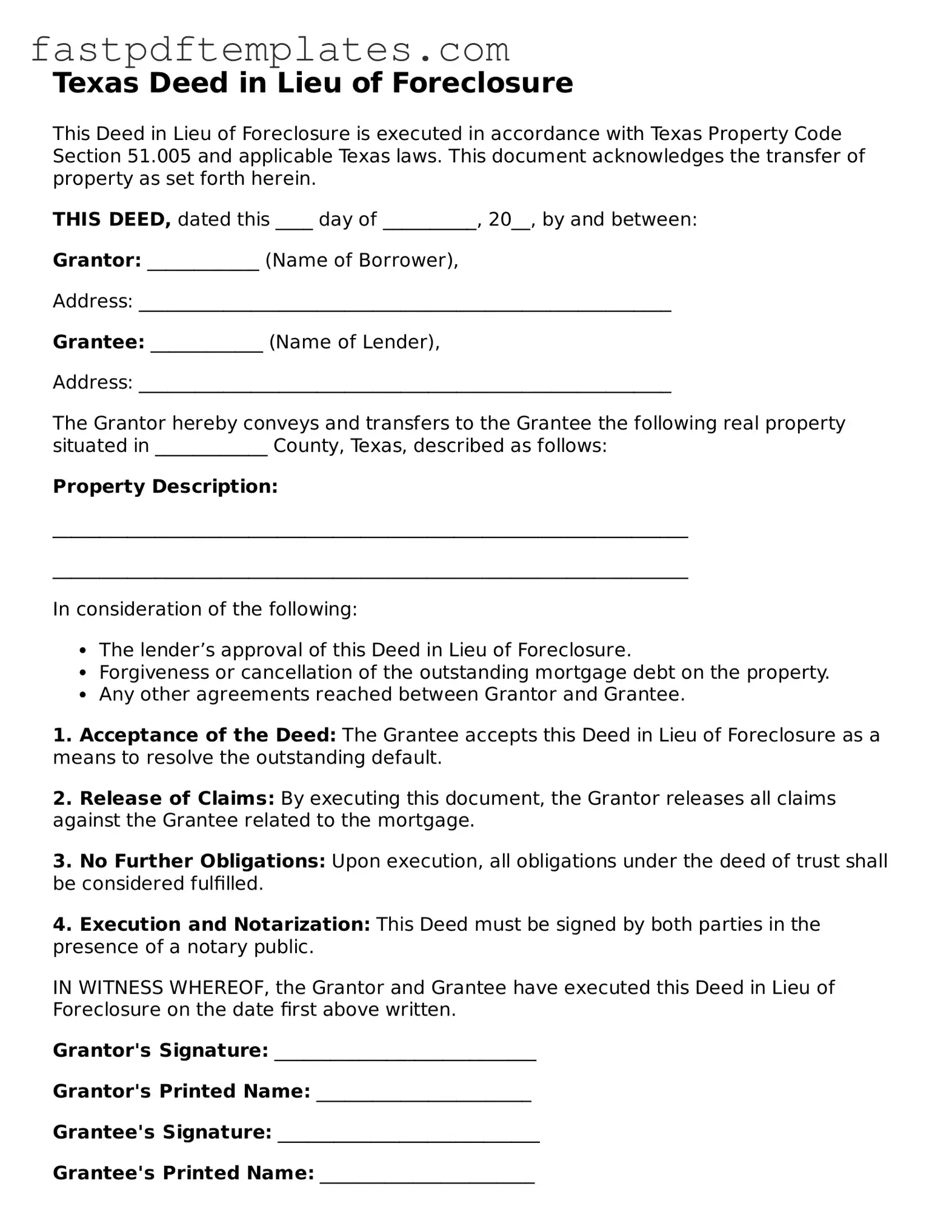

This Deed in Lieu of Foreclosure is executed in accordance with Texas Property Code Section 51.005 and applicable Texas laws. This document acknowledges the transfer of property as set forth herein.

THIS DEED, dated this ____ day of __________, 20__, by and between:

Grantor: ____________ (Name of Borrower),

Address: _________________________________________________________

Grantee: ____________ (Name of Lender),

Address: _________________________________________________________

The Grantor hereby conveys and transfers to the Grantee the following real property situated in ____________ County, Texas, described as follows:

Property Description:

____________________________________________________________________

____________________________________________________________________

In consideration of the following:

1. Acceptance of the Deed: The Grantee accepts this Deed in Lieu of Foreclosure as a means to resolve the outstanding default.

2. Release of Claims: By executing this document, the Grantor releases all claims against the Grantee related to the mortgage.

3. No Further Obligations: Upon execution, all obligations under the deed of trust shall be considered fulfilled.

4. Execution and Notarization: This Deed must be signed by both parties in the presence of a notary public.

IN WITNESS WHEREOF, the Grantor and Grantee have executed this Deed in Lieu of Foreclosure on the date first above written.

Grantor's Signature: ____________________________

Grantor's Printed Name: _______________________

Grantee's Signature: ____________________________

Grantee's Printed Name: _______________________

State of Texas

County of ______________

SUBSCRIBED AND SWORN to before me on this ____ day of ____________, 20__.

Notary Public in and for the State of Texas

My Commission Expires: ________________

Deed in Lieu Vs Foreclosure - A property inspection may be required before the transfer to assess its condition.

Deed in Lieu Vs Foreclosure - This option gives borrowers a chance to put an end to their mortgage struggles peacefully.

When filling out the Texas Deed in Lieu of Foreclosure form, it is important to follow certain guidelines to ensure the process goes smoothly. Here are some dos and don'ts to keep in mind:

When filling out and using the Texas Deed in Lieu of Foreclosure form, consider the following key takeaways:

Taking these steps can help ensure a smoother process when using the Texas Deed in Lieu of Foreclosure form.

The Texas Deed in Lieu of Foreclosure is similar to a mortgage modification agreement. In both cases, the borrower and lender work together to find a solution that avoids foreclosure. A mortgage modification agreement involves changing the terms of the existing loan, such as reducing the interest rate or extending the repayment period. This can help borrowers who are struggling to make their payments by making their loan more manageable. The goal is to keep the borrower in their home while ensuring that the lender can still recover their investment. Both documents aim to provide a more favorable outcome for the borrower while protecting the lender’s interests.

Another document that shares similarities with the Texas Deed in Lieu of Foreclosure is the short sale agreement. In a short sale, the homeowner sells the property for less than what is owed on the mortgage, with the lender’s consent. Like the deed in lieu, a short sale is an alternative to foreclosure that allows the borrower to avoid the negative consequences associated with losing their home. Both options require the lender's approval and involve negotiations to determine the best course of action for all parties involved. Ultimately, both documents aim to minimize losses for the lender while providing the borrower with a way to move forward financially.

A third document that bears resemblance to the Texas Deed in Lieu of Foreclosure is the foreclosure forbearance agreement. This agreement allows borrowers to temporarily pause their mortgage payments due to financial hardship, providing them with time to recover. Similar to a deed in lieu, a forbearance agreement is intended to help borrowers avoid foreclosure. It grants them the opportunity to catch up on missed payments or work out a long-term solution with the lender. Both documents reflect a collaborative effort between the borrower and lender to address financial difficulties while aiming to preserve homeownership whenever possible.

Lastly, the assumption of mortgage agreement is another document that aligns closely with the Texas Deed in Lieu of Foreclosure. In an assumption agreement, a new buyer takes over the existing mortgage from the seller, which can be a viable option when the seller is facing foreclosure. This document allows the seller to transfer their mortgage obligations to someone else, potentially preventing foreclosure and allowing the lender to recoup their investment. Both the assumption of mortgage and deed in lieu represent alternatives to foreclosure, providing pathways for borrowers and lenders to navigate challenging financial situations while minimizing losses.

A Texas Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer their property back to the lender to avoid foreclosure. When engaging in this process, several other forms and documents may be necessary to ensure a smooth transaction. Below is a list of these documents, each serving a specific purpose.

Having these documents ready can streamline the process and help avoid complications. Always consult with a legal professional for guidance tailored to your specific situation.