Fillable Promissory Note for a Car Document

Fillable Promissory Note for a Car Document

Understanding a Promissory Note for a Car can be challenging. Here are ten common misconceptions about this important document:

Once you have the Promissory Note for a Car form ready, it’s time to fill it out accurately. This document is crucial for establishing the terms of the loan for your vehicle purchase. Follow these steps to complete the form correctly.

After filling out the form, review it for accuracy. Ensure all information is correct before submitting it to the lender. Keep a copy for your records as well.

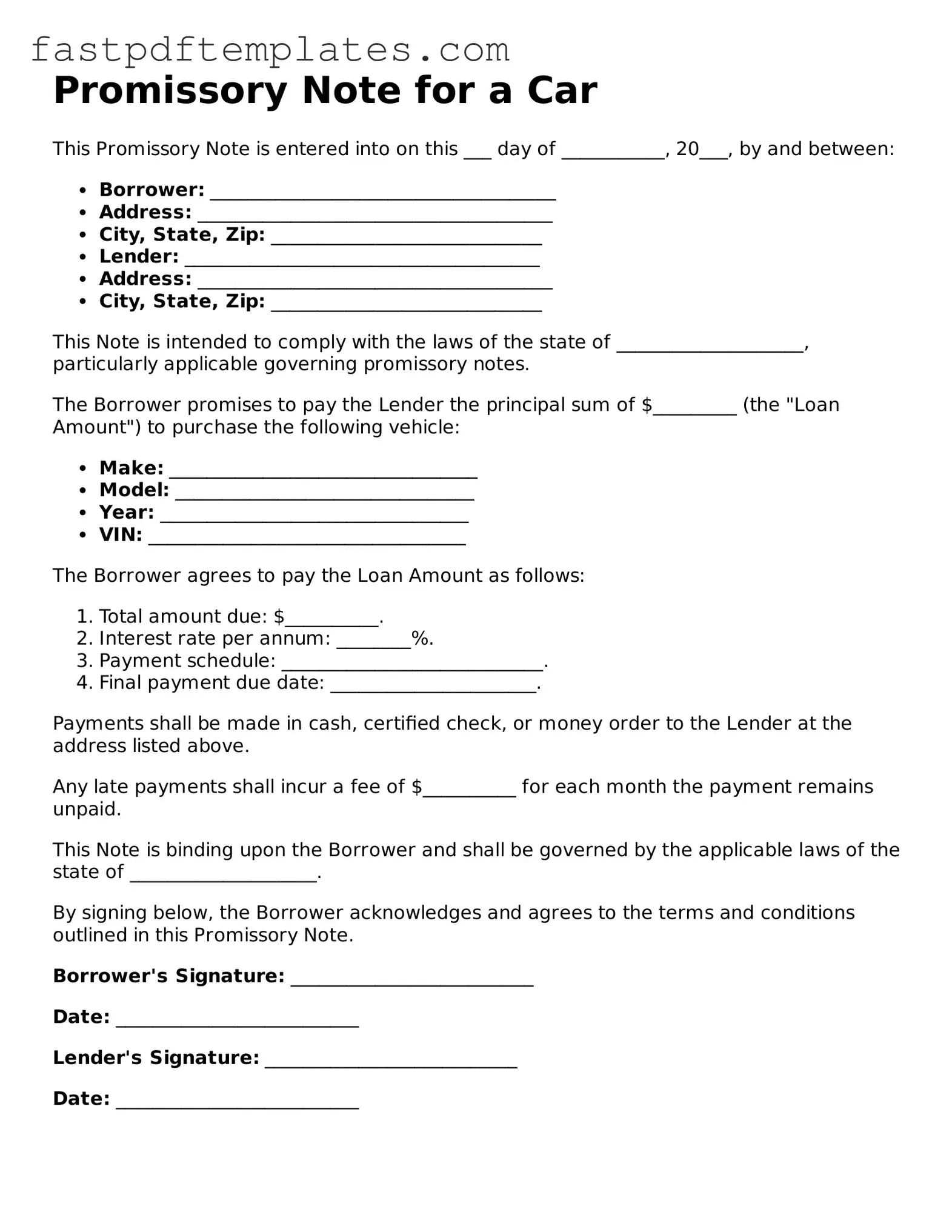

Promissory Note for a Car

This Promissory Note is entered into on this ___ day of ___________, 20___, by and between:

This Note is intended to comply with the laws of the state of ____________________, particularly applicable governing promissory notes.

The Borrower promises to pay the Lender the principal sum of $_________ (the "Loan Amount") to purchase the following vehicle:

The Borrower agrees to pay the Loan Amount as follows:

Payments shall be made in cash, certified check, or money order to the Lender at the address listed above.

Any late payments shall incur a fee of $__________ for each month the payment remains unpaid.

This Note is binding upon the Borrower and shall be governed by the applicable laws of the state of ____________________.

By signing below, the Borrower acknowledges and agrees to the terms and conditions outlined in this Promissory Note.

Borrower's Signature: __________________________

Date: __________________________

Lender's Signature: ___________________________

Date: __________________________

Promissory Note Release - Allows for a clean financial slate for the borrower.

When filling out the Promissory Note for a Car form, it is important to ensure accuracy and clarity. Here are some guidelines to follow:

When dealing with the Promissory Note for a Car, understanding its components and implications is crucial. Here are some key takeaways to consider:

A Promissory Note for a Car is quite similar to a Loan Agreement. Both documents serve as a formal promise to repay borrowed money. A Loan Agreement typically outlines the terms of the loan, including the interest rate, repayment schedule, and any collateral involved. Like a Promissory Note, it binds the borrower to repay the lender under specified conditions. However, a Loan Agreement may also include additional clauses about default, which can provide more comprehensive protection for the lender.

Another document that shares similarities with a Promissory Note for a Car is a Mortgage. While a Mortgage is specifically tied to real estate, both documents establish a borrower-lender relationship and outline repayment terms. In a Mortgage, the property itself serves as collateral, similar to how a car may be secured by the Promissory Note. Both documents are legally binding and can lead to significant consequences if the borrower fails to meet their obligations.

A Retail Installment Sale Contract is also comparable to a Promissory Note for a Car. This document is often used in vehicle purchases, detailing the terms of financing directly between a buyer and a seller. Like a Promissory Note, it specifies the purchase price, interest rate, and payment schedule. The key difference lies in the fact that a Retail Installment Sale Contract may include the seller’s right to repossess the vehicle if payments are not made, providing an added layer of security for the seller.

Lastly, a Credit Agreement bears resemblance to a Promissory Note for a Car. This document outlines the terms under which a borrower can access credit from a lender. Similar to a Promissory Note, it includes details about the amount borrowed, repayment terms, and interest rates. However, Credit Agreements often cover broader financial arrangements and may allow for multiple transactions over time, whereas a Promissory Note typically focuses on a single loan for a specific purpose, such as purchasing a vehicle.

When entering into a financing agreement for a car, several important documents accompany the Promissory Note for a Car. Each of these documents plays a crucial role in outlining the terms of the sale and the responsibilities of both the buyer and the seller. Understanding these forms can help ensure a smooth transaction.

By familiarizing yourself with these documents, you can navigate the car buying process with confidence. Each form contributes to a transparent and legally sound transaction, helping to protect both the buyer and seller.