Blank Profit And Loss Form

Blank Profit And Loss Form

Understanding the Profit and Loss (P&L) form is essential for anyone involved in managing finances, whether for a business or personal budgeting. However, several misconceptions can lead to confusion. Here are seven common misunderstandings:

By clarifying these misconceptions, individuals and businesses can better utilize the Profit and Loss form to enhance their financial understanding and decision-making.

Filling out a Profit and Loss form is an important step in understanding the financial health of a business. By accurately completing this form, individuals and businesses can gain insights into their revenues, expenses, and overall profitability. Below are the steps to guide you through the process of filling out the form.

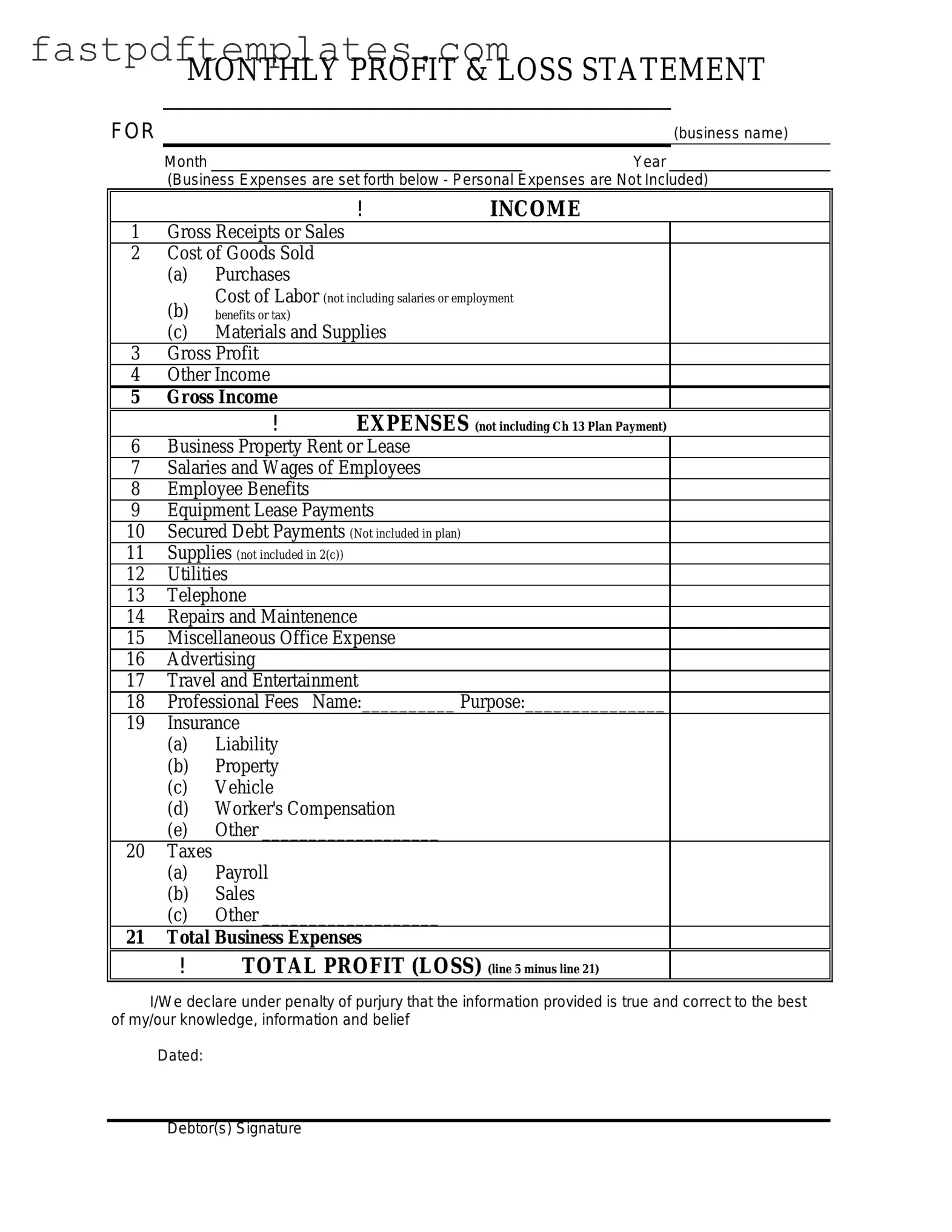

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

Cg2010 - Insurance provided under this endorsement is limited to the scope required by existing contracts.

Esa Approval - The document helps ensure that individuals can live and travel with their emotional support animals.

Consolation Bracket - Strategy is key to navigating through the bracket.

When filling out a Profit and Loss form, it's important to approach the task with care. Here are some key do's and don'ts to keep in mind:

By following these guidelines, you can create a clear and accurate Profit and Loss statement that reflects your business's financial health.

Filling out and using the Profit and Loss form is essential for understanding a business's financial performance. Here are some key takeaways:

The Profit and Loss statement, often referred to as the income statement, is similar to the balance sheet. Both documents provide insights into a company's financial health. While the Profit and Loss statement focuses on revenues and expenses over a specific period, the balance sheet offers a snapshot of assets, liabilities, and equity at a single point in time. Together, they give a comprehensive view of a company's financial situation.

The cash flow statement is another document that shares similarities with the Profit and Loss statement. Both track financial performance, but they focus on different aspects. The Profit and Loss statement details income and expenses, while the cash flow statement shows how cash moves in and out of the business. This document highlights the company's liquidity, which is crucial for day-to-day operations.

A budget report is also akin to the Profit and Loss statement. A budget outlines expected revenues and expenses, serving as a financial plan for the future. The Profit and Loss statement, on the other hand, reflects actual performance over a period. Comparing the two helps businesses identify variances and adjust their strategies accordingly.

The trial balance report is another document that relates closely to the Profit and Loss statement. It lists all the accounts in the general ledger along with their balances. This report serves as a preliminary check to ensure that total debits equal total credits. While the Profit and Loss statement summarizes income and expenses, the trial balance provides the detailed account balances that support those figures.

The statement of retained earnings is similar in that it connects to the Profit and Loss statement through net income. This document explains how profits are retained in the business or distributed as dividends. It starts with the previous period's retained earnings, adds net income from the Profit and Loss statement, and subtracts any dividends paid out.

The sales report shares a connection with the Profit and Loss statement as well. This document provides detailed information about sales performance over a specific period. While the Profit and Loss statement summarizes total revenues, the sales report breaks down sales by product, region, or other categories, giving a more granular view of income generation.

An expense report is another document that parallels the Profit and Loss statement. It provides a detailed account of all expenses incurred by a business during a specific period. The Profit and Loss statement aggregates these expenses to show total costs. Both documents are essential for understanding where money is spent and how it affects overall profitability.

The accounts receivable aging report is similar because it tracks outstanding invoices. This document categorizes receivables based on how long they have been outstanding. While the Profit and Loss statement reflects revenue earned, the aging report shows how much of that revenue is still pending collection, impacting cash flow and financial planning.

Lastly, the annual report includes the Profit and Loss statement as part of its financial disclosures. This comprehensive document provides stakeholders with an overview of the company's performance over the year. It typically includes the Profit and Loss statement, balance sheet, cash flow statement, and management's discussion, giving a complete picture of the company's financial health and strategic direction.

The Profit and Loss form is a crucial document for any business, providing a snapshot of financial performance over a specific period. However, several other forms and documents complement this report, offering a more comprehensive view of the company’s financial health. Below is a list of these essential documents.

Understanding these documents alongside the Profit and Loss form enables businesses to make informed financial decisions. Each document plays a vital role in presenting a complete picture of financial health and operational efficiency.