Attorney-Approved New York Loan Agreement Document

Attorney-Approved New York Loan Agreement Document

Many people have misunderstandings about the New York Loan Agreement form. Here are five common misconceptions:

Loan agreements can vary significantly based on the type of loan, the lender, and the borrower. The New York Loan Agreement form is tailored to meet specific state laws and requirements.

Even small loans benefit from a formal agreement. A written contract helps clarify terms and protects both parties, regardless of the loan amount.

While verbal agreements may seem convenient, they are often hard to enforce. A written loan agreement provides clear documentation of the terms and conditions.

Terms can be modified if both parties agree to the changes. It is important to document any amendments in writing to avoid confusion later.

The New York Loan Agreement form can be used for various types of loans, including personal, business, and real estate loans. It is versatile and adaptable.

Filling out the New York Loan Agreement form is an important step in securing your loan. It’s essential to provide accurate information to ensure a smooth process. Once you've completed the form, you will be one step closer to finalizing your loan agreement.

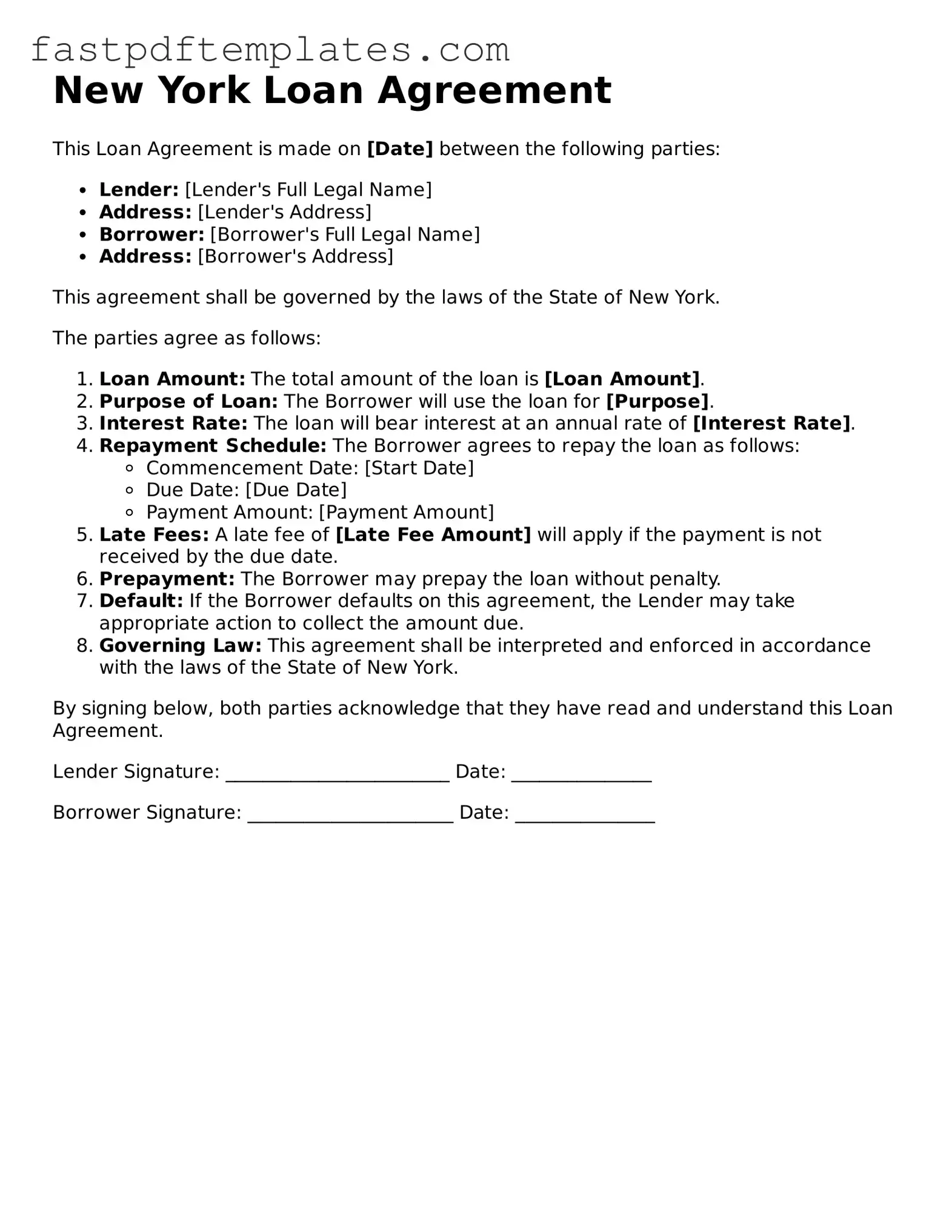

New York Loan Agreement

This Loan Agreement is made on [Date] between the following parties:

This agreement shall be governed by the laws of the State of New York.

The parties agree as follows:

By signing below, both parties acknowledge that they have read and understand this Loan Agreement.

Lender Signature: ________________________ Date: _______________

Borrower Signature: ______________________ Date: _______________

Promissory Note Texas - It may incorporate any state-specific lending regulations.

Loan Agreement Template Georgia - The agreement reinforces the lender’s right to collect payments.

Loan Agreement Template California - Consideration of state regulations may influence the agreement's provisions.

When filling out the New York Loan Agreement form, attention to detail is crucial. Here are eight important dos and don'ts to consider:

Filling out and using the New York Loan Agreement form requires attention to detail and an understanding of its components. Here are four key takeaways to consider:

The New York Loan Agreement form shares similarities with a Promissory Note. Both documents outline the terms of a loan, detailing the amount borrowed, interest rates, and repayment schedules. A Promissory Note serves as a written promise by the borrower to repay the loan, while the Loan Agreement provides a more comprehensive framework that includes additional terms and conditions. In essence, the Promissory Note is often a component of the broader Loan Agreement, reinforcing the borrower's commitment to repay the debt.

Another document that resembles the New York Loan Agreement is a Security Agreement. This document is used when a borrower pledges collateral to secure a loan. Like the Loan Agreement, it specifies the rights and obligations of both parties. The Security Agreement ensures that if the borrower defaults, the lender can seize the collateral. Both documents work together to protect the lender's interests while defining the terms of the borrowing arrangement.

The New York Loan Agreement also has parallels with a Mortgage Agreement. A Mortgage Agreement is specifically related to real estate transactions and outlines the terms under which a borrower can obtain financing to purchase property. Similar to the Loan Agreement, it includes details about the loan amount, interest rate, and repayment terms. However, the Mortgage Agreement adds provisions regarding the property itself, establishing it as collateral for the loan. Both documents aim to create a clear understanding of the borrowing terms and the consequences of default.

Lastly, the New York Loan Agreement can be compared to a Line of Credit Agreement. This document allows borrowers to access funds up to a specified limit, with the flexibility to draw on the credit as needed. Like the Loan Agreement, it sets forth the terms of borrowing, including interest rates and repayment expectations. However, a Line of Credit Agreement typically offers more flexibility in terms of borrowing and repayment, making it distinct yet similar in its foundational purpose of facilitating access to funds.

When entering into a loan agreement in New York, several additional documents may be required to ensure clarity and protect the interests of all parties involved. Each of these documents serves a specific purpose and helps to facilitate a smooth transaction.

Understanding these documents can help borrowers navigate the loan process more effectively. Each plays a crucial role in defining the terms of the loan and protecting the rights of all parties involved.