Blank IRS 2553 Form

Blank IRS 2553 Form

The IRS Form 2553 is a crucial document for small business owners who wish to elect S corporation status. However, several misconceptions surround this form that can lead to confusion and missteps. Below are six common misunderstandings:

This is not true. Existing businesses can also file Form 2553 to change their tax status to an S corporation.

While filing the form is necessary, the IRS must approve the application. Failure to meet eligibility requirements can result in denial.

In fact, the form must be filed within a specific time frame, typically within 75 days of the beginning of the tax year for which the election is to take effect.

This is partially correct. While S corporations can only have U.S. citizens or residents as shareholders, there are specific exceptions for certain trusts and estates.

This is misleading. While S corporation status can reduce self-employment taxes on distributions, it does not eliminate them entirely. Salaries paid to shareholders are still subject to these taxes.

This is incorrect. A business can revoke its S corporation status by filing a statement with the IRS, but there are specific procedures and consequences to consider.

Filling out the IRS Form 2553 is an important step for certain businesses electing to be treated as an S corporation for tax purposes. After completing the form, it should be submitted to the IRS to ensure the desired tax status is recognized. Below are the steps to accurately fill out the form.

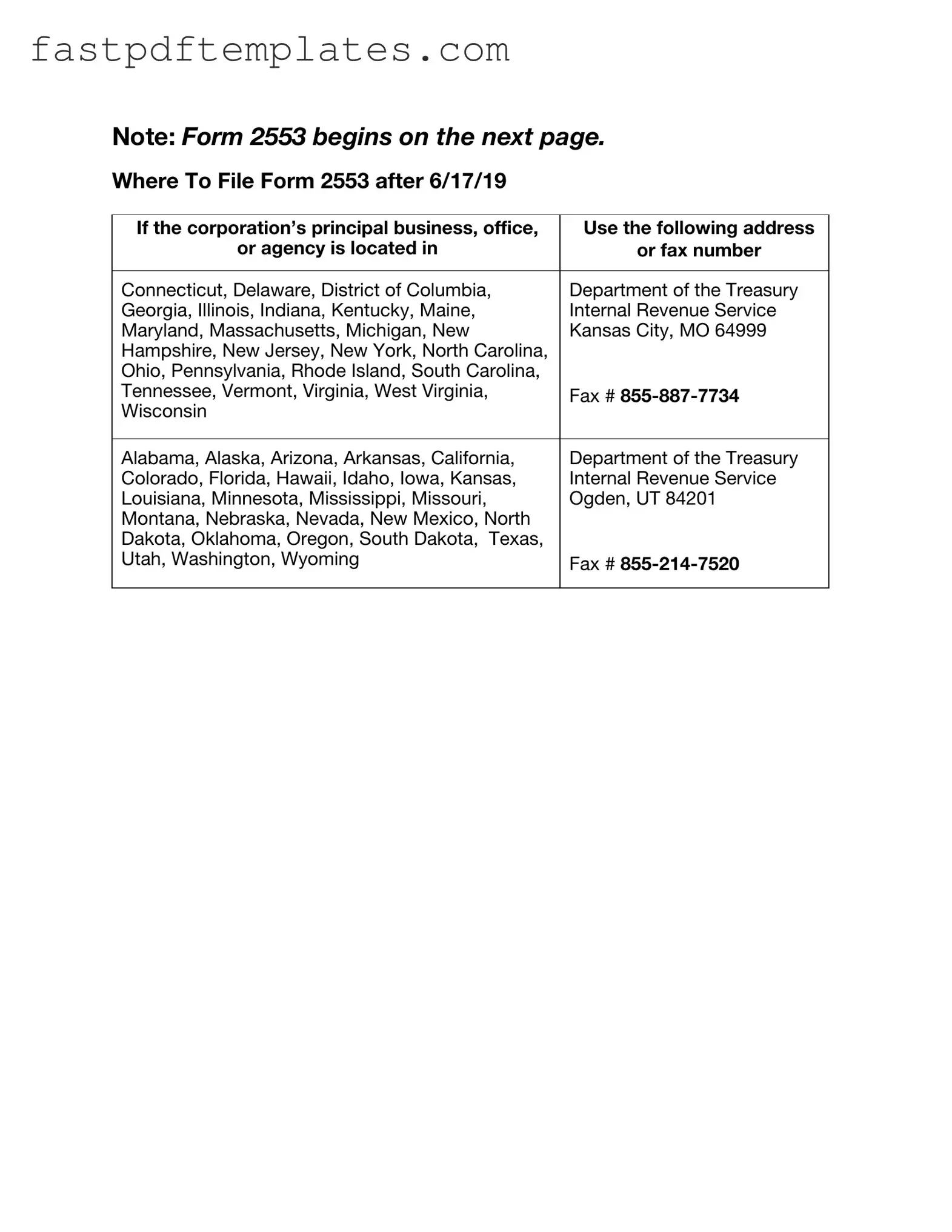

Note: Form 2553 begins on the next page.

Where To File Form 2553 after 6/17/19

If the corporation’s principal business, office, |

Use the following address |

or agency is located in |

or fax number |

|

|

Connecticut, Delaware, District of Columbia, |

Department of the Treasury |

Georgia, Illinois, Indiana, Kentucky, Maine, |

Internal Revenue Service |

Maryland, Massachusetts, Michigan, New |

Kansas City, MO 64999 |

Hampshire, New Jersey, New York, North Carolina, |

|

Ohio, Pennsylvania, Rhode Island, South Carolina, |

|

Tennessee, Vermont, Virginia, West Virginia, |

Fax # |

Wisconsin |

|

|

|

Alabama, Alaska, Arizona, Arkansas, California, |

Department of the Treasury |

Colorado, Florida, Hawaii, Idaho, Iowa, Kansas, |

Internal Revenue Service |

Louisiana, Minnesota, Mississippi, Missouri, |

Ogden, UT 84201 |

Montana, Nebraska, Nevada, New Mexico, North |

|

Dakota, Oklahoma, Oregon, South Dakota, Texas, |

|

Utah, Washington, Wyoming |

Fax # |

|

|

Form 2553

(Rev. December 2017)

Department of the Treasury Internal Revenue Service

Election by a Small Business Corporation

(Under section 1362 of the Internal Revenue Code)

(Including a late election filed pursuant to Rev. Proc.

▶You can fax this form to the IRS. See separate instructions.

▶Go to www.irs.gov/Form2553 for instructions and the latest information.

OMB No.

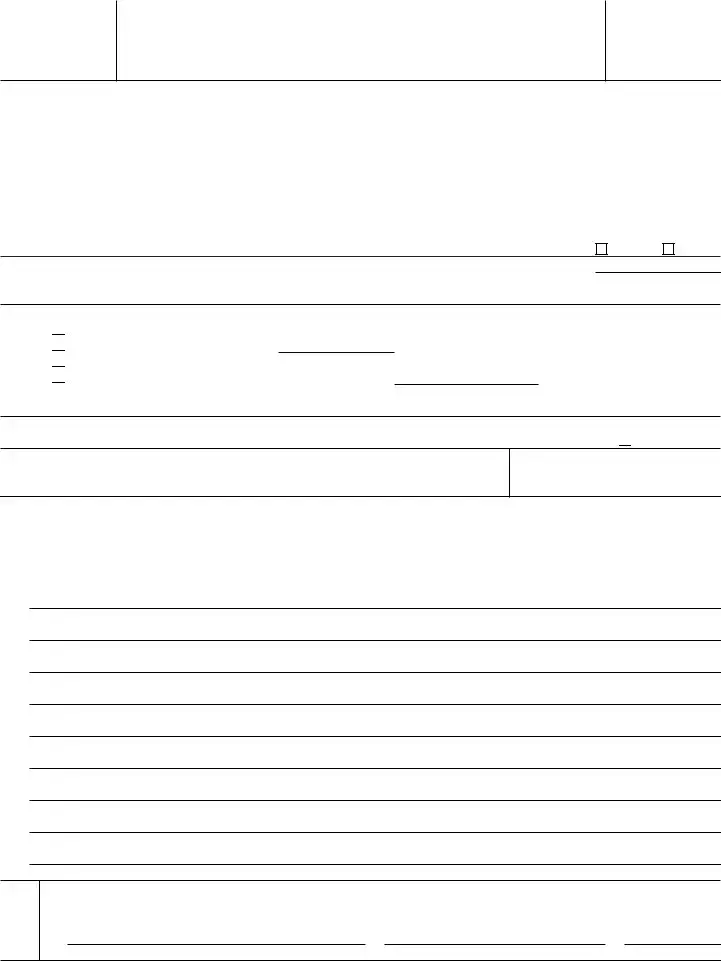

Note: This election to be an S corporation can be accepted only if all the tests are met under Who May Elect in the instructions, all shareholders have signed the consent statement, an officer has signed below, and the exact name and address of the corporation (entity) and other required form information have been provided.

Part I |

|

Election Information |

|

|

|

|

|

|

|

Name (see instructions) |

A Employer identification number |

||

Type |

|

|

|

|

|

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

B Date incorporated |

|

|||

or |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

||

|

City or town, state or province, country, and ZIP or foreign postal code |

C State of incorporation |

|

|||

|

|

|

|

|||

|

|

|

|

|

|

|

D |

Check |

the applicable box(es) if the corporation (entity), after applying for the EIN shown in A above, changed its |

name or |

address |

||

EElection is to be effective for tax year beginning (month, day, year) (see instructions) . . . . . . ▶

Caution: A corporation (entity) making the election for its first tax year in existence will usually enter the beginning date of a short tax year that begins on a date other than January 1.

FSelected tax year:

(1) Calendar year

Calendar year

(2) Fiscal year ending (month and day) ▶

Fiscal year ending (month and day) ▶

(3)

(4)

If box (2) or (4) is checked, complete Part II.

GIf more than 100 shareholders are listed for item J (see page 2), check this box if treating members of a family as one shareholder results in no more than 100 shareholders (see test 2 under Who May Elect in the instructions) ▶

HName and title of officer or legal representative whom the IRS may call for more information

Telephone number of officer or legal representative

IIf this S corporation election is being filed late, I declare I had reasonable cause for not filing Form 2553 timely. If this late election is being made by an entity eligible to elect to be treated as a corporation, I declare I also had reasonable cause for not filing an entity classification election timely and the representations listed in Part IV are true. See below for my explanation of the reasons the election or elections were not made on time and a description of my diligent actions to correct the mistake upon its discovery. See instructions.

|

Under penalties of perjury, I declare that I have examined this election, including accompanying documents, and, to the best of my |

||

Sign knowledge and belief, the election contains all the relevant facts relating to the election, and such facts are true, correct, and complete. |

|||

Here |

▲Signature of officer |

|

|

|

Title |

Date |

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 18629R |

Form 2553 (Rev. |

|

Form 2553 (Rev. |

Page 2 |

Name |

Employer identification number |

Part I Election Information (continued) Note: If you need more rows, use additional copies of page 2.

J

Name and address of each

shareholder or former shareholder required to consent to the election.

(see instructions)

K

Shareholder’s Consent Statement

Under penalties of perjury, I declare that I consent to the election of the

Signature |

Date |

L

Stock owned or

percentage of ownership

(see instructions)

Number of |

|

shares or |

|

percentage |

Date(s) |

of ownership |

acquired |

M |

|

Social security |

|

number or |

N |

employer |

Shareholder’s |

identification |

tax year ends |

number (see |

(month and |

instructions) |

day) |

Form 2553 (Rev.

Form 2553 (Rev. |

Page 3 |

|

Name |

|

Employer identification number |

|

|

|

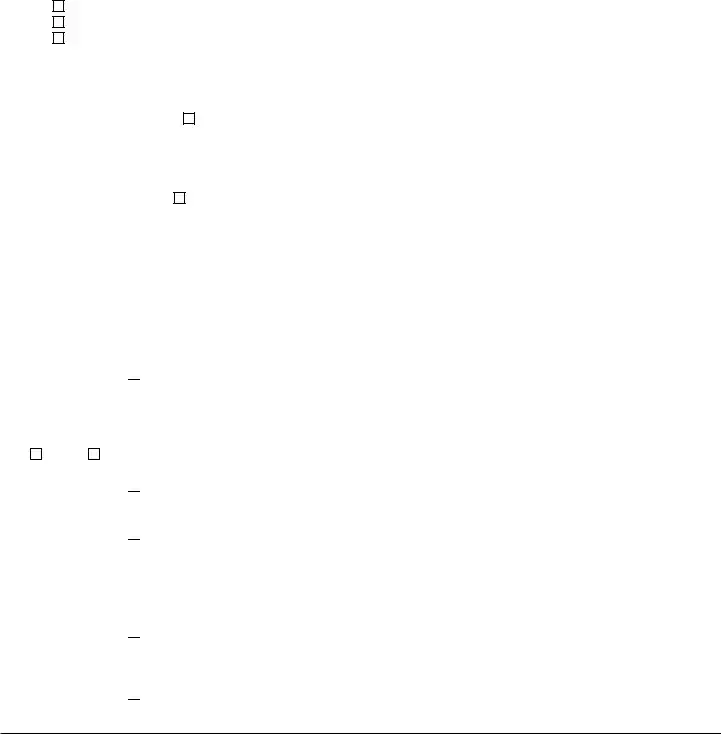

Part II |

Selection of Fiscal Tax Year (see instructions) |

|

Note: All corporations using this part must complete item O and item P, Q, or R. |

|

|

O Check the applicable box to indicate whether the corporation is: |

|

|

1. |

A new corporation adopting the tax year entered in item F, Part I. |

|

2. |

An existing corporation retaining the tax year entered in item F, Part I. |

|

3. |

An existing corporation changing to the tax year entered in item F, Part I. |

|

PComplete item P if the corporation is using the automatic approval provisions of Rev. Proc.

1. Natural Business Year ▶ |

I represent that the corporation is adopting, retaining, or changing to a tax year that qualifies |

as its natural business year (as defined in section 5.07 of Rev. Proc.

2. Ownership Tax Year ▶ |

I represent that shareholders (as described in section 5.08 of Rev. Proc. |

than half of the shares of the stock (as of the first day of the tax year to which the request relates) of the corporation have the same tax year or are concurrently changing to the tax year that the corporation adopts, retains, or changes to per item F, Part I, and that such tax year satisfies the requirement of section 4.01(3) of Rev. Proc.

Note: If you do not use item P and the corporation wants a fiscal tax year, complete either item Q or R below. Item Q is used to request a fiscal tax year based on a business purpose and to make a

QBusiness

1. Check here ▶  if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

if the fiscal year entered in item F, Part I, is requested under the prior approval provisions of Rev. Proc.

Yes |

No |

2.Check here ▶

to show that the corporation intends to make a

to show that the corporation intends to make a

3.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event (1) the corporation’s business purpose request is not approved and the corporation makes a

RSection 444

1.Check here ▶

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

to show that the corporation will make, if qualified, a section 444 election to have the fiscal tax year shown in item F, Part I. To make the election, you must complete Form 8716, Election To Have a Tax Year Other Than a Required Tax Year, and either attach it to Form 2553 or file it separately.

2.Check here ▶

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

to show that the corporation agrees to adopt or change to a tax year ending December 31 if necessary for the IRS to accept this election for S corporation status in the event the corporation is ultimately not qualified to make a section 444 election.

Form 2553 (Rev.

Form 2553 (Rev. |

Page 4 |

Name |

Employer identification number |

Part III Qualified Subchapter S Trust (QSST) Election Under Section 1361(d)(2)* Note: If you are making more than

one QSST election, use additional copies of page 4.

Income beneficiary’s name and address

Social security number

Trust’s name and address

Employer identification number

Date on which stock of the corporation was transferred to the trust (month, day, year) . . . . . . . . ▶

In order for the trust named above to be a QSST and thus a qualifying shareholder of the S corporation for which this Form 2553 is filed, I hereby make the election under section 1361(d)(2). Under penalties of perjury, I certify that the trust meets the definitional requirements of section 1361(d)(3) and that all other information provided in Part III is true, correct, and complete.

Signature of income beneficiary or signature and title of legal representative or other qualified person making the election |

|

Date |

*Use Part III to make the QSST election only if stock of the corporation has been transferred to the trust on or before the date on which the corporation makes its election to be an S corporation. The QSST election must be made and filed separately if stock of the corporation is transferred to the trust after the date on which the corporation makes the S election.

Part IV Late Corporate Classification Election Representations (see instructions)

If a late entity classification election was intended to be effective on the same date that the S corporation election was intended to be effective, relief for a late S corporation election must also include the following representations.

1The requesting entity is an eligible entity as defined in Regulations section

2The requesting entity intended to be classified as a corporation as of the effective date of the S corporation status;

3The requesting entity fails to qualify as a corporation solely because Form 8832, Entity Classification Election, was not timely filed under Regulations section

4The requesting entity fails to qualify as an S corporation on the effective date of the S corporation status solely because the S corporation election was not timely filed pursuant to section 1362(b); and

5a The requesting entity timely filed all required federal tax returns and information returns consistent with its requested classification as an S corporation for all of the years the entity intended to be an S corporation and no inconsistent tax or information returns have been filed by or with respect to the entity during any of the tax years, or

bThe requesting entity has not filed a federal tax or information return for the first year in which the election was intended to be effective because the due date has not passed for that year’s federal tax or information return.

Form 2553 (Rev.

Lyft Inspection Form Pass - Your commitment to vehicular safety is highlighted through consistent inspections.

Employer's Quarterly Federal Tax Return - The due date for Form 941 is typically the last day of the month following the quarter.

Filling out the IRS Form 2553 can be a crucial step for small business owners looking to elect S Corporation status. To ensure a smooth process, here are some important do's and don'ts to keep in mind.

By following these guidelines, you can help ensure that your Form 2553 is completed correctly and submitted without any hiccups.

When filling out and using the IRS Form 2553, there are several important points to keep in mind. This form is essential for businesses that want to elect S corporation status. Here are some key takeaways:

The IRS Form 8832 is similar to Form 2553 in that both are used by entities to elect their tax classification. While Form 2553 is specifically for S Corporations, Form 8832 allows businesses to choose how they want to be classified for federal tax purposes, whether as a corporation, partnership, or sole proprietorship. This flexibility can significantly impact the tax obligations of a business, making the choice crucial for effective financial planning.

Form 1065, the U.S. Return of Partnership Income, is another document that shares similarities with Form 2553. While Form 2553 is used to elect S Corporation status, Form 1065 is filed by partnerships to report their income, deductions, and other important financial information. Both forms require detailed information about the entity’s structure and operations, reflecting the importance of accurate reporting for tax compliance.

The IRS Form 1120 is the U.S. Corporation Income Tax Return, which parallels Form 2553 in its focus on corporate tax obligations. Form 1120 is filed by C Corporations to report their income, gains, losses, and deductions. While Form 2553 is about electing S Corporation status, both forms are integral to understanding a corporation's tax responsibilities, albeit under different classifications.

Form 941, the Employer's Quarterly Federal Tax Return, also bears resemblance to Form 2553. Both forms are essential for businesses, particularly those with employees. Form 941 is used to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks, while Form 2553 is crucial for electing S Corporation status, which can affect how these taxes are calculated and reported.

The IRS Form 1065-B, the Return of Income for Electing Large Partnerships, is another document that shares similarities with Form 2553. Like Form 2553, which allows a corporation to elect S status, Form 1065-B is specifically designed for large partnerships that choose to be taxed under a special set of rules. Both forms require specific elections to be made for tax treatment, emphasizing the importance of entity classification.

Form 1120-S, the U.S. Income Tax Return for an S Corporation, is directly linked to Form 2553. Once a business elects S Corporation status using Form 2553, it must file Form 1120-S annually to report its income, deductions, and other tax-related information. This connection highlights the importance of Form 2553 in determining the tax obligations of S Corporations.

Form W-2, the Wage and Tax Statement, is another document that, while different in purpose, has a connection to Form 2553. Businesses that elect S Corporation status must issue Form W-2 to their employees to report wages and taxes withheld. Both forms play critical roles in ensuring accurate tax reporting and compliance for businesses with employees.

The IRS Form 1040, the U.S. Individual Income Tax Return, is also relevant in this context. While Form 2553 is focused on corporate elections, the individual tax return is where shareholders of S Corporations report their share of the corporation’s income. This relationship underscores the impact of Form 2553 on individual tax obligations for those involved in S Corporations.

Form 720, the Quarterly Federal Excise Tax Return, shares a thematic connection with Form 2553 in that both are used for tax reporting purposes. While Form 720 is specifically for reporting excise taxes, businesses that elect S Corporation status using Form 2553 must also ensure compliance with various tax obligations, including any applicable excise taxes.

Lastly, Form 8862, the Information to Claim Earned Income Credit After Disallowance, is relevant in the broader context of tax compliance. Although it serves a different purpose, it highlights the importance of accurate reporting and eligibility requirements, much like Form 2553 does for S Corporations. Both forms require careful attention to detail to ensure compliance with IRS regulations.

The IRS Form 2553 is essential for small businesses electing to be taxed as an S corporation. However, several other forms and documents often accompany it to ensure compliance with federal and state regulations. Here is a list of those documents, each serving a specific purpose in the process.

Filing the IRS Form 2553 and the accompanying documents is crucial for maintaining the S corporation status. Each form plays a role in ensuring compliance with tax regulations and protecting the interests of the business and its shareholders.