Attorney-Approved Illinois Loan Agreement Document

Attorney-Approved Illinois Loan Agreement Document

Understanding the Illinois Loan Agreement form is crucial for both lenders and borrowers. However, several misconceptions can lead to confusion. Here are six common misunderstandings:

Many people believe that all loan agreements follow the same format and terms. In reality, each loan agreement can vary significantly based on the type of loan, the parties involved, and specific state laws. The Illinois Loan Agreement form has its unique requirements and stipulations that must be adhered to.

Some individuals think that simply signing the loan agreement guarantees they will receive the funds. However, the agreement is a promise to lend or borrow under specified terms, and the actual disbursement of funds may depend on additional factors such as creditworthiness or collateral.

There is a misconception that verbal agreements can replace written contracts. While oral agreements may hold some weight, they are often difficult to enforce. A written loan agreement provides clear documentation of the terms, which helps protect both parties.

Some people think the Illinois Loan Agreement form is exclusively for personal loans. In fact, it can be used for various types of loans, including business loans, student loans, and more. Its versatility makes it applicable in numerous lending situations.

Many believe that after signing the loan agreement, the terms are set in stone. However, amendments can be made if both parties agree. It is essential to document any changes in writing to maintain clarity and enforceability.

Some individuals may feel intimidated by the legal language in loan agreements. However, the Illinois Loan Agreement form is designed to be straightforward. Understanding the key components can help borrowers and lenders navigate the process with confidence.

After obtaining the Illinois Loan Agreement form, it is important to complete it accurately to ensure all parties understand their obligations. This process involves filling out various sections of the form with the relevant information. Follow the steps below to fill out the form correctly.

Once the form is completed, it should be reviewed for accuracy. After ensuring that all information is correct, both parties should keep a copy for their records. This will help in maintaining transparency and accountability throughout the loan period.

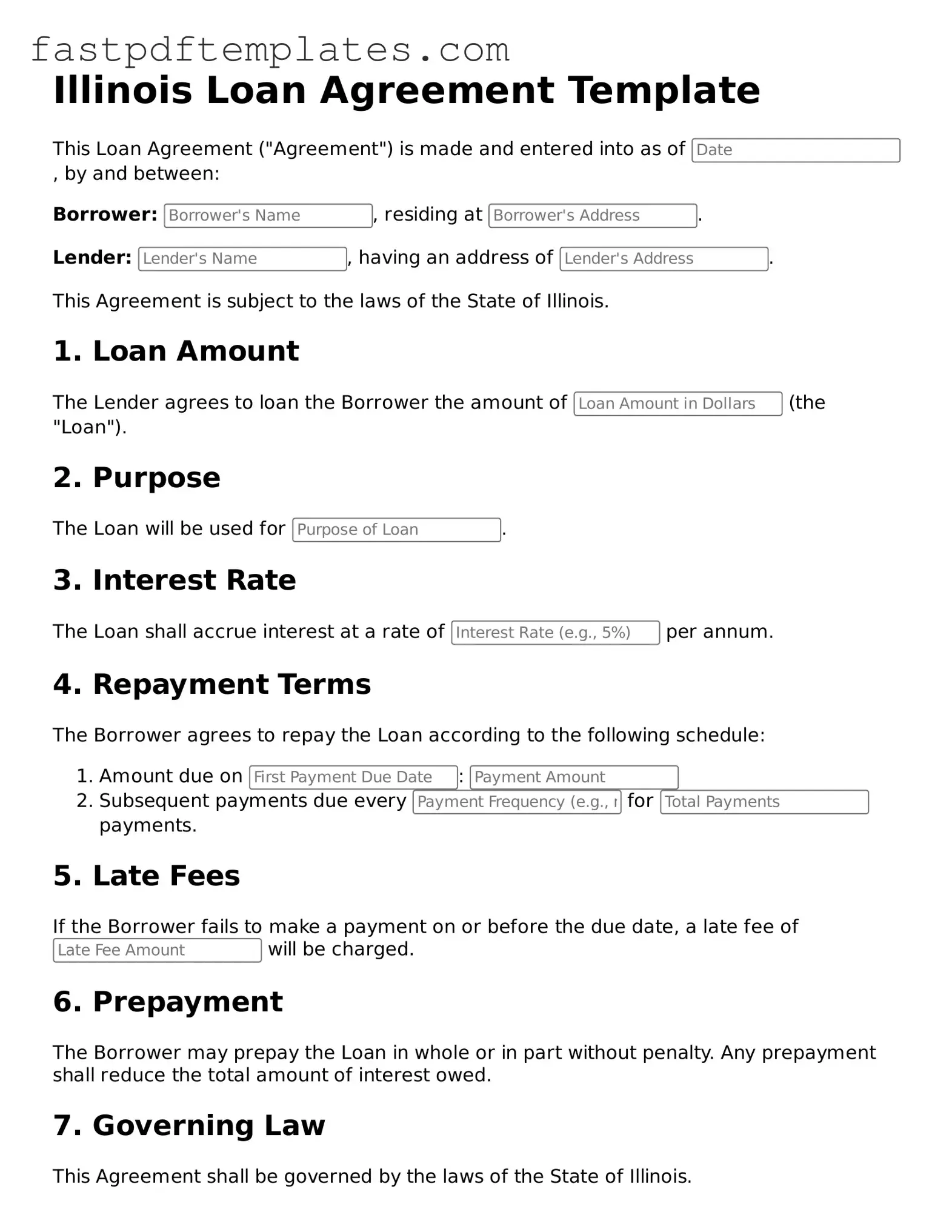

Illinois Loan Agreement Template

This Loan Agreement ("Agreement") is made and entered into as of , by and between:

Borrower: , residing at .

Lender: , having an address of .

This Agreement is subject to the laws of the State of Illinois.

1. Loan Amount

The Lender agrees to loan the Borrower the amount of (the "Loan").

2. Purpose

The Loan will be used for .

3. Interest Rate

The Loan shall accrue interest at a rate of per annum.

4. Repayment Terms

The Borrower agrees to repay the Loan according to the following schedule:

5. Late Fees

If the Borrower fails to make a payment on or before the due date, a late fee of will be charged.

6. Prepayment

The Borrower may prepay the Loan in whole or in part without penalty. Any prepayment shall reduce the total amount of interest owed.

7. Governing Law

This Agreement shall be governed by the laws of the State of Illinois.

8. Signatures

By signing below, both parties agree to the terms outlined in this Loan Agreement.

Borrower's Signature: ___________________________ Date: ________________

Lender's Signature: ___________________________ Date: ________________

Promissory Note Texas - It describes the lender's rights to inspect the borrower's records.

Loan Agreement Template California - After both parties sign, the agreement becomes legally binding.

When filling out the Illinois Loan Agreement form, it’s important to approach the task with care. Here’s a list of things you should and shouldn’t do to ensure the process goes smoothly.

When dealing with the Illinois Loan Agreement form, it is essential to understand its components and requirements. Here are key takeaways to consider:

Understanding these elements will facilitate a smoother process in filling out and utilizing the Illinois Loan Agreement form.

The Illinois Loan Agreement form shares similarities with a promissory note. A promissory note is a written promise to pay a specific amount of money at a designated time or on demand. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedules. While the loan agreement may provide more detailed terms and conditions, the promissory note serves as a simpler, straightforward acknowledgment of the debt.

Another document that resembles the Illinois Loan Agreement is a security agreement. A security agreement outlines the terms under which collateral is provided to secure a loan. Similar to the loan agreement, it details the obligations of the borrower and the lender. Both documents aim to protect the lender’s interests in case of default, ensuring that they have a claim to the collateral specified in the security agreement.

The Illinois Loan Agreement is also comparable to a mortgage agreement. A mortgage agreement specifically relates to real estate transactions, where the property serves as collateral for the loan. Both documents include terms regarding the loan amount, interest rate, and repayment schedule. However, the mortgage agreement typically contains additional provisions related to property ownership and responsibilities, reflecting the nature of real estate financing.

A lease agreement is another document that shares some characteristics with the Illinois Loan Agreement. While primarily used for renting property, a lease agreement outlines the terms of payment and obligations between the landlord and tenant. Like a loan agreement, it specifies the duration of the agreement, payment amounts, and conditions for termination. Both documents establish a legal framework for financial transactions between parties.

A line of credit agreement also bears resemblance to the Illinois Loan Agreement. This document allows a borrower to access funds up to a specified limit, similar to how a loan agreement outlines the amount borrowed. Both agreements detail repayment terms and interest rates, although a line of credit may offer more flexibility in how funds are accessed and repaid over time.

The Illinois Loan Agreement can be compared to a personal loan agreement. This type of agreement specifies the terms of borrowing money for personal use, such as consolidating debt or financing a purchase. Both documents outline the loan amount, interest rate, and repayment schedule. The primary difference lies in the intended use of the funds, with personal loans often being unsecured.

A business loan agreement is similar to the Illinois Loan Agreement, particularly when used for financing business operations. This document outlines the terms of borrowing for business purposes, including interest rates and repayment schedules. Both agreements serve to formalize the lender-borrower relationship, ensuring clarity on the obligations and expectations of both parties.

A credit card agreement also shares elements with the Illinois Loan Agreement. This document outlines the terms under which a credit card issuer extends credit to a cardholder. Both agreements specify interest rates, payment terms, and fees. However, credit card agreements often include more variable terms, reflecting the revolving nature of credit card debt.

A debt settlement agreement is another document that can be likened to the Illinois Loan Agreement. This agreement outlines the terms under which a debtor agrees to settle a debt for less than the full amount owed. Both documents detail the obligations of the parties involved, although a debt settlement agreement typically involves negotiation and compromise, while a loan agreement establishes clear terms for repayment.

Lastly, a forbearance agreement can be compared to the Illinois Loan Agreement. This document allows a borrower to temporarily postpone payments on a loan, often due to financial hardship. Both agreements address the terms of repayment, including any adjustments to the repayment schedule. The forbearance agreement serves as a way to provide relief to the borrower while maintaining the lender’s rights to the debt.

When entering into a loan agreement in Illinois, it's essential to understand the other documents that may accompany the main contract. These forms help clarify the terms of the loan, protect the interests of both parties, and ensure compliance with state laws. Below is a list of commonly used forms and documents that often accompany an Illinois Loan Agreement.

Understanding these documents can empower borrowers and lenders alike, fostering a clearer and more transparent lending process. Each form plays a vital role in protecting the interests of both parties and ensuring that the loan is managed effectively throughout its term.