Blank Gift Letter Form

Blank Gift Letter Form

When it comes to the Gift Letter form, there are several misconceptions that can lead to confusion. Understanding these myths can help ensure a smoother process when it comes to receiving or giving a financial gift, especially in the context of real estate transactions.

By clearing up these misconceptions, individuals can navigate the process of giving and receiving gifts with greater confidence and clarity.

Filling out a Gift Letter form is an important step in documenting the transfer of funds as a gift. This process ensures clarity and transparency for both the giver and the recipient, particularly in financial contexts such as mortgage applications. Following these steps will help ensure that the form is completed accurately and efficiently.

Once the form is filled out completely, it can be submitted to the relevant parties, such as a lender or financial institution, as part of the documentation for the financial transaction. Ensure that both the donor and recipient keep a copy for their records.

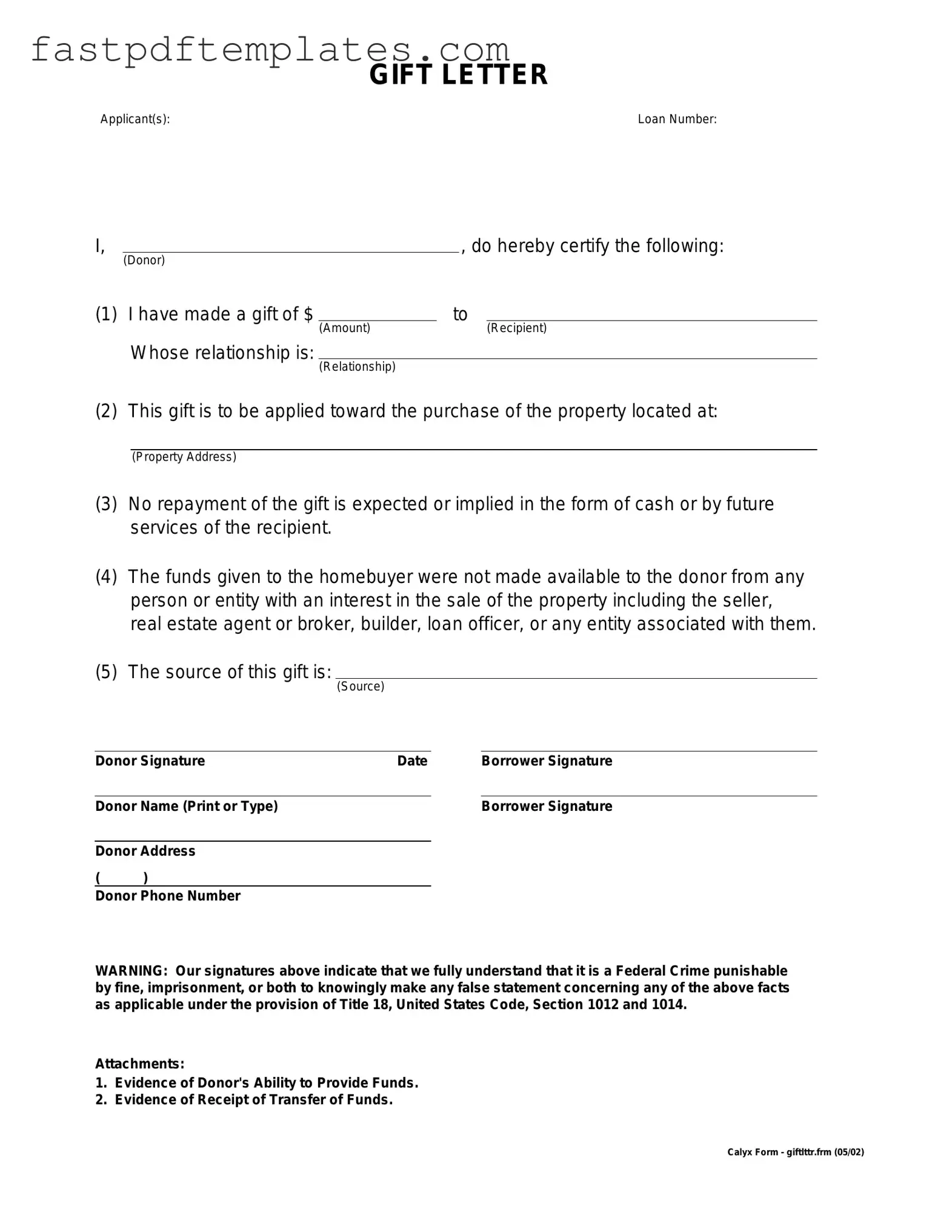

GIFT LETTER

Applicant(s): |

Loan Number: |

I, |

|

|

, do hereby certify the following: |

||

|

(Donor) |

|

|

|

|

(1) I have made a gift of $ |

|

to |

|

||

|

|

(Amount) |

|

|

(Recipient) |

|

Whose relationship is: |

|

|

|

|

|

|

(Relationship) |

|

|

|

(2) This gift is to be applied toward the purchase of the property located at:

(Property Address)

(3)No repayment of the gift is expected or implied in the form of cash or by future services of the recipient.

(4)The funds given to the homebuyer were not made available to the donor from any person or entity with an interest in the sale of the property including the seller, real estate agent or broker, builder, loan officer, or any entity associated with them.

(5)The source of this gift is:

(Source)

Donor Signature |

Date |

Borrower Signature |

||

|

|

|

|

|

Donor Name (Print or Type) |

|

|

Borrower Signature |

|

|

|

|

|

|

Donor Address |

|

|

|

|

( |

) |

|

|

|

Donor Phone Number

WARNING: Our signatures above indicate that we fully understand that it is a Federal Crime punishable by fine, imprisonment, or both to knowingly make any false statement concerning any of the above facts as applicable under the provision of Title 18, United States Code, Section 1012 and 1014.

Attachments:

1.Evidence of Donor's Ability to Provide Funds.

2.Evidence of Receipt of Transfer of Funds.

Calyx Form - giftlttr.frm (05/02)

U.S. Corporation Income Tax Return - The 1120 form is a key element in the financial reporting process for U.S. corporations.

What Does a Job Application Look Like - Indicate the city in which you reside.

Parent Consent Letter for Travel - Mandatory for all minors sailing unaccompanied, the form ensures smooth travel arrangements.

When filling out a Gift Letter form, it's important to approach the task with care. This document can play a significant role in various financial transactions, particularly in real estate. Here are some helpful guidelines to follow:

When filling out and using a Gift Letter form, several important considerations can help ensure clarity and compliance. Here are some key takeaways:

The Gift Letter form is similar to a Loan Agreement. Both documents serve to outline the terms of a financial transaction. In a Loan Agreement, the borrower agrees to repay borrowed funds, while a Gift Letter confirms that the funds provided are a gift and do not require repayment. Clarity in both documents is essential to avoid misunderstandings regarding the financial relationship between the parties involved.

Another document comparable to the Gift Letter form is the Affidavit of Support. This document is often used in immigration cases to demonstrate that a sponsor can financially support an immigrant. Like the Gift Letter, it asserts that the funds are available for use without any expectation of repayment. Both documents provide assurance to third parties, such as lenders or immigration authorities, about the financial support being offered.

The Promissory Note is also similar in that it involves a financial agreement. However, a Promissory Note indicates that the borrower agrees to repay a specified amount of money, typically with interest. In contrast, the Gift Letter explicitly states that the funds are a gift and do not require repayment. This distinction is crucial for those involved in transactions requiring clear documentation of financial intentions.

A Quitclaim Deed shares similarities with the Gift Letter in terms of transferring ownership. This document is often used to transfer property rights without guaranteeing that the title is free of claims. In both cases, the intention is to convey something of value without expecting anything in return. This can be particularly relevant in familial situations where property is transferred as a gift.

The Financial Gift Declaration is another document that resembles the Gift Letter. It serves to declare the nature of a financial gift, often in a legal context. Both documents articulate that the funds provided are a gift, emphasizing the absence of repayment obligations. This helps to clarify the intent behind the transfer of funds, which can be important for tax purposes.

A Charitable Donation Receipt is similar in that it acknowledges a transfer of funds, but it typically involves a donation to a nonprofit organization. While the Gift Letter is personal and may involve family or friends, both documents confirm that the funds are given without expectation of return. They serve as proof of the transaction for record-keeping and tax deduction purposes.

The Inheritance Document also shares characteristics with the Gift Letter. This document outlines the transfer of assets from a deceased individual to their heirs. Similar to a gift, inheritance does not involve repayment. Both documents serve to clarify the nature of the transfer and the intentions behind it, which can be significant for legal and tax implications.

A Release of Liability form can be compared to the Gift Letter in terms of relinquishing claims. While a Release of Liability typically protects one party from future claims related to an activity, the Gift Letter releases the giver from any obligation to reclaim the gifted funds. Both documents help establish clear boundaries and intentions regarding financial transactions.

The Memorandum of Understanding (MOU) can also be seen as similar to the Gift Letter. An MOU outlines an agreement between parties, often regarding a mutual understanding or intention. While it may not be legally binding, it clarifies the expectations of both parties. The Gift Letter similarly clarifies the expectations surrounding a financial gift, ensuring that both parties understand the nature of the transaction.

Finally, the Bill of Sale is another document that bears resemblance to the Gift Letter. A Bill of Sale serves as a record of the transfer of ownership of personal property. While it typically involves a sale, it can also document a gift of property. Both documents serve to confirm the transfer of something of value without the expectation of repayment, highlighting the intent behind the transaction.

When preparing a Gift Letter for a financial transaction, several other forms and documents may be required to ensure a smooth process. Each of these documents serves a specific purpose and helps clarify the nature of the gift, the parties involved, and the financial implications. Below is a list of commonly used forms that often accompany a Gift Letter.

Gathering these documents alongside the Gift Letter can facilitate a clearer understanding of the financial transaction. Each document plays a vital role in verifying the details of the gift and ensuring compliance with legal and financial regulations.