Attorney-Approved Georgia Promissory Note Document

Attorney-Approved Georgia Promissory Note Document

Understanding the Georgia Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are ten common misconceptions:

Being aware of these misconceptions can help you navigate the use of promissory notes more effectively.

After obtaining the Georgia Promissory Note form, it's important to carefully fill it out to ensure all necessary information is included. This process will help create a legally binding document between the borrower and lender. Follow these steps to complete the form accurately.

Once the form is completed, both parties should keep a copy for their records. This ensures that everyone has access to the terms agreed upon in the promissory note.

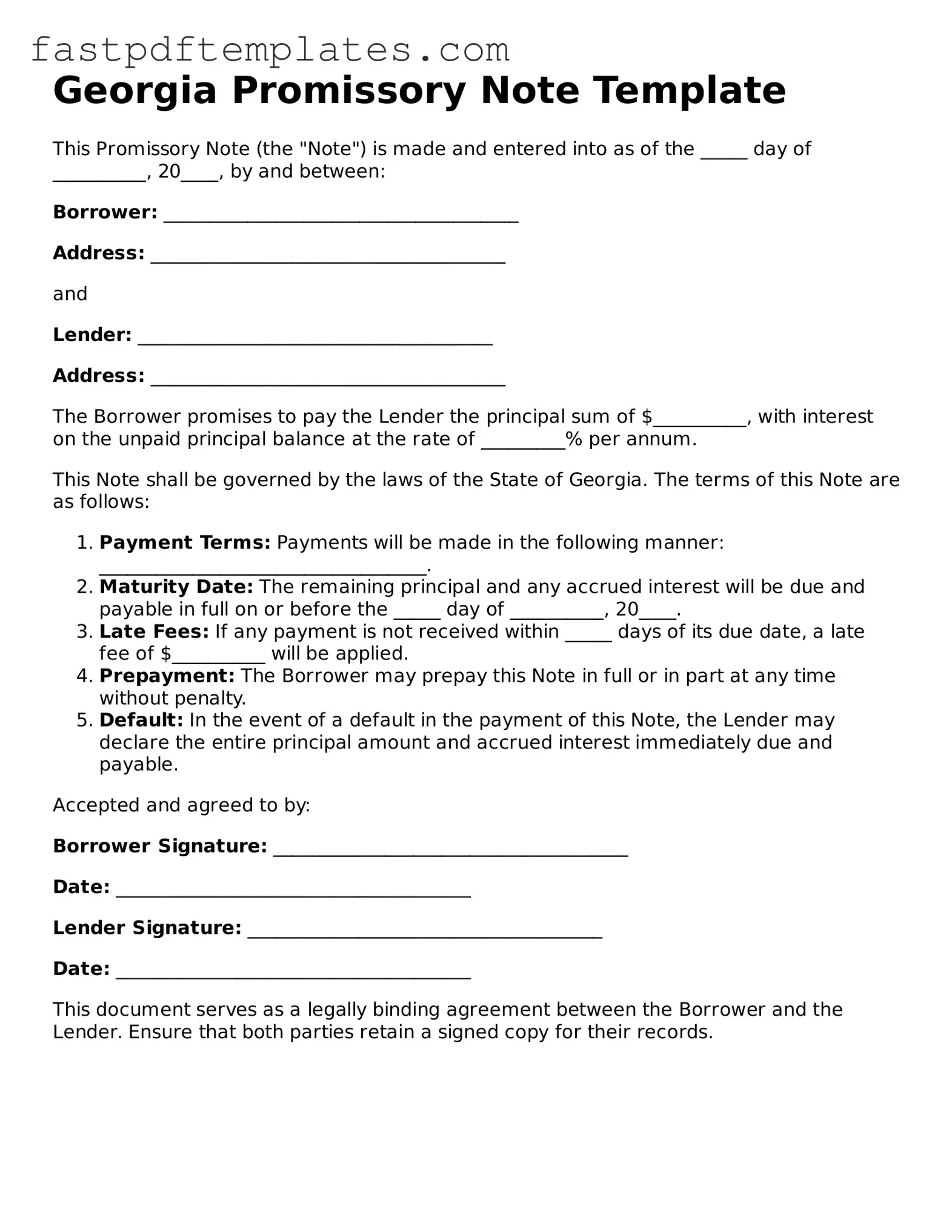

Georgia Promissory Note Template

This Promissory Note (the "Note") is made and entered into as of the _____ day of __________, 20____, by and between:

Borrower: ______________________________________

Address: ______________________________________

and

Lender: ______________________________________

Address: ______________________________________

The Borrower promises to pay the Lender the principal sum of $__________, with interest on the unpaid principal balance at the rate of _________% per annum.

This Note shall be governed by the laws of the State of Georgia. The terms of this Note are as follows:

Accepted and agreed to by:

Borrower Signature: ______________________________________

Date: ______________________________________

Lender Signature: ______________________________________

Date: ______________________________________

This document serves as a legally binding agreement between the Borrower and the Lender. Ensure that both parties retain a signed copy for their records.

California Promissory Note Requirements - Acts as an official record of the debt owed.

Promissory Note New York - This form helps clarify the obligations of both parties.

Illinois Promissory Note - It can be drafted for various amounts, big or small, ensuring flexibility in lending.

Texas Promissory Note - In certain cases, a promissory note can also include provisions for prepayment.

When filling out the Georgia Promissory Note form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here is a list of things you should and shouldn't do:

Filling out and using the Georgia Promissory Note form requires attention to detail and an understanding of its key components. Here are nine essential takeaways:

These takeaways can help ensure that the promissory note is filled out correctly and serves its intended purpose in a legal context.

A loan agreement is a document that outlines the terms and conditions of a loan between a borrower and a lender. Like a promissory note, it specifies the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement often includes additional details such as collateral, default terms, and legal rights of both parties. This makes it a more comprehensive document compared to a promissory note, which primarily focuses on the borrower's promise to repay the loan.

A mortgage is a specific type of loan agreement used to finance the purchase of real estate. It involves a promissory note, but also includes a security interest in the property. If the borrower defaults, the lender can take possession of the property through foreclosure. This distinguishes a mortgage from a standard promissory note, as the latter does not typically involve collateral tied to the loan.

An IOU is an informal document acknowledging a debt. While a promissory note is a formal, legally binding agreement, an IOU is often less detailed and may not include terms such as interest rates or repayment schedules. Both documents signify that money is owed, but an IOU lacks the legal enforceability and structure of a promissory note.

A personal guarantee is a document where an individual agrees to be responsible for a debt or obligation if the primary borrower defaults. Similar to a promissory note, it creates a financial obligation. However, a personal guarantee is usually used in business contexts and serves to protect the lender by holding an individual accountable for a business's debts.

A secured note is similar to a promissory note but includes collateral to back the loan. This means that if the borrower fails to repay, the lender has the right to claim the collateral. The presence of collateral provides additional security to the lender, making a secured note more favorable in high-risk lending situations compared to a standard promissory note.

A business loan agreement is tailored for loans taken out by businesses rather than individuals. Like a promissory note, it details the amount borrowed and repayment terms. However, it also encompasses specific business-related clauses, such as covenants that the business must adhere to during the term of the loan. This makes it more complex than a typical promissory note.

An installment agreement outlines a payment plan for settling a debt over time. It shares similarities with a promissory note in that it specifies payment amounts and schedules. However, an installment agreement often includes provisions for penalties or fees for late payments, which may not be explicitly detailed in a simple promissory note.

A lease agreement can resemble a promissory note when it includes terms for payment of rent. Both documents establish a payment obligation. However, a lease agreement is more comprehensive, covering the terms of property use, maintenance responsibilities, and duration of the lease, while a promissory note focuses solely on the repayment of borrowed funds.

A credit agreement is a broader document that outlines the terms under which credit will be extended to a borrower. It includes details about repayment terms, interest rates, and fees, similar to a promissory note. However, a credit agreement may also include clauses regarding credit limits and conditions for borrowing, making it more detailed than a standard promissory note.

A debt settlement agreement is a document that outlines the terms under which a debtor agrees to pay a reduced amount to settle a debt. Like a promissory note, it creates an obligation to pay. However, it often involves negotiation and may include terms for a lump-sum payment or a structured payment plan, which distinguishes it from the straightforward promise of repayment found in a promissory note.

The Georgia Promissory Note is a crucial document for establishing the terms of a loan agreement between a borrower and a lender. However, several other forms and documents often accompany it to ensure clarity and protection for both parties involved. Below is a list of these commonly used documents.

Utilizing these documents in conjunction with the Georgia Promissory Note can help clarify the terms of the loan and protect the interests of both the borrower and lender. Each form serves a specific purpose, contributing to a well-structured loan agreement.