Attorney-Approved Florida Promissory Note Document

Attorney-Approved Florida Promissory Note Document

When it comes to the Florida Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these misconceptions can help ensure that all parties involved are on the same page. Here are four common misunderstandings:

This is not true. While notarization can add an extra layer of authenticity, a promissory note does not require a notary to be legally binding in Florida. As long as the note includes the essential elements, it is valid.

Many people think these two documents are interchangeable. However, a promissory note is a simpler document that outlines the promise to pay a specific amount of money. In contrast, a loan agreement typically includes more detailed terms and conditions, such as repayment schedules and collateral.

This is incorrect. Parties can agree to modify the terms of a promissory note after it has been signed. However, any changes should be documented in writing and signed by all parties involved to ensure clarity and avoid disputes.

Many believe that promissory notes are only necessary for substantial amounts of money. In reality, they can be used for any loan amount, whether large or small. The important factor is that both parties understand the terms of repayment.

After you have gathered all necessary information, you are ready to fill out the Florida Promissory Note form. This document will require specific details about the loan agreement, including the parties involved, the amount borrowed, and repayment terms.

Once the form is completed, ensure that both parties retain a copy for their records. It is advisable to keep the original in a safe place, as it serves as a legal record of the agreement.

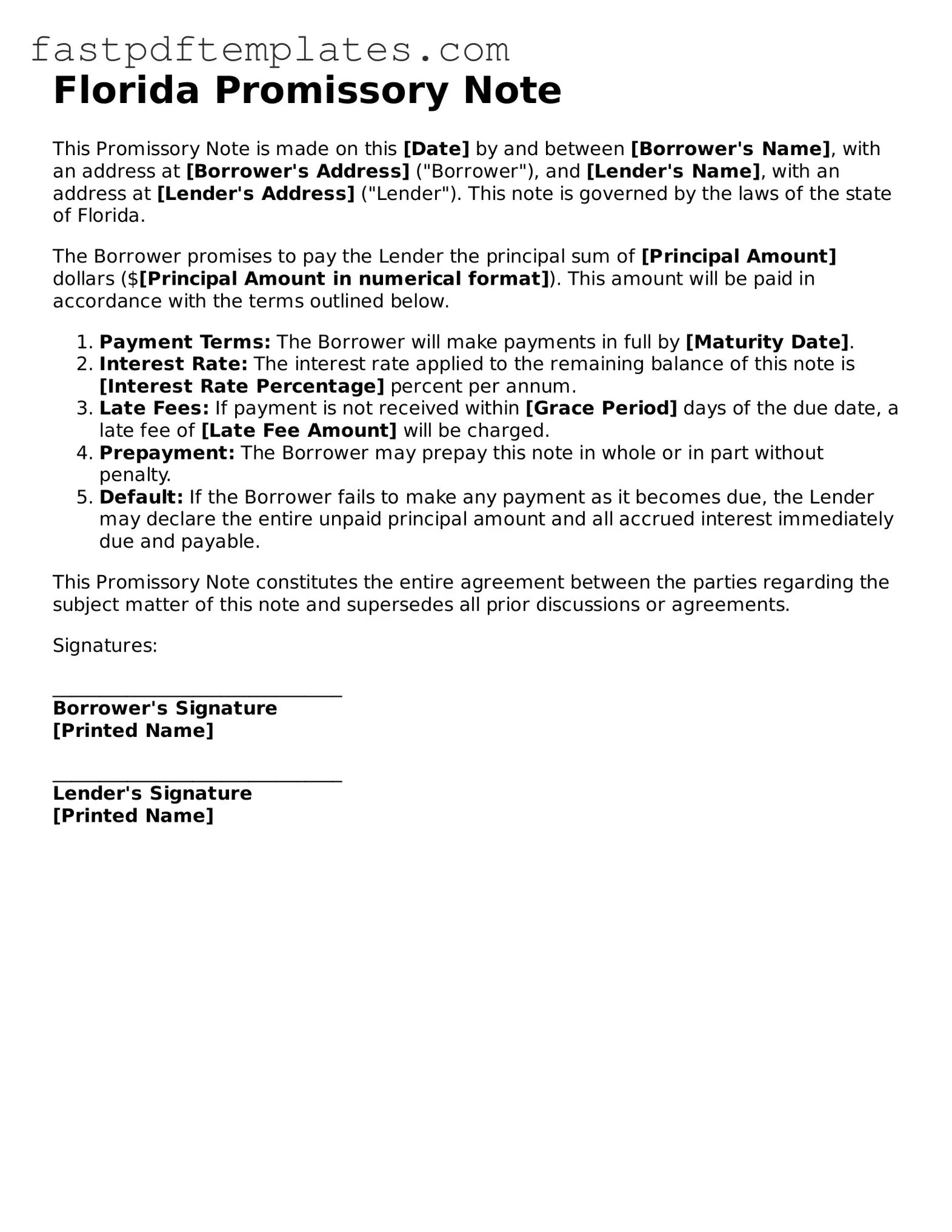

Florida Promissory Note

This Promissory Note is made on this [Date] by and between [Borrower's Name], with an address at [Borrower's Address] ("Borrower"), and [Lender's Name], with an address at [Lender's Address] ("Lender"). This note is governed by the laws of the state of Florida.

The Borrower promises to pay the Lender the principal sum of [Principal Amount] dollars ($[Principal Amount in numerical format]). This amount will be paid in accordance with the terms outlined below.

This Promissory Note constitutes the entire agreement between the parties regarding the subject matter of this note and supersedes all prior discussions or agreements.

Signatures:

_______________________________

Borrower's Signature

[Printed Name]

_______________________________

Lender's Signature

[Printed Name]

Promissory Note Georgia - Revocation or modification of terms usually requires mutual consent of both parties.

Texas Promissory Note - Whether it’s a personal or business transaction, it's important to have a written agreement.

California Promissory Note Requirements - Ensures both parties understand their rights and responsibilities.

When filling out the Florida Promissory Note form, attention to detail is crucial. Here are some essential dos and don'ts to guide you through the process.

Filling out and using the Florida Promissory Note form requires attention to detail and understanding of key components. Here are ten important takeaways:

By keeping these key points in mind, you can effectively navigate the process of creating and using a Florida Promissory Note.

A Florida Promissory Note is similar to a Loan Agreement. Both documents serve the purpose of outlining the terms of a loan between a borrower and a lender. They specify the amount borrowed, the interest rate, and the repayment schedule. However, a Loan Agreement often includes additional details such as collateral, default conditions, and other legal obligations, making it a more comprehensive document. In contrast, a Promissory Note is typically more straightforward and focuses primarily on the borrower's promise to repay the loan.

Another document akin to the Florida Promissory Note is a Mortgage. While a Promissory Note represents the borrower's commitment to repay a loan, a Mortgage secures that loan with real property. This means if the borrower defaults, the lender has the right to take possession of the property. Both documents are essential in real estate transactions, but the Mortgage provides the lender with a legal claim to the property, adding an extra layer of security compared to a standalone Promissory Note.

A Security Agreement also shares similarities with a Promissory Note. Both documents involve a borrower and a lender, outlining terms of a loan. However, a Security Agreement specifically details collateral that secures the loan, which can be personal property or other assets. In contrast, the Promissory Note primarily focuses on the borrower's obligation to repay the loan, without necessarily detailing the collateral. This distinction is crucial for lenders when assessing the risk of the loan.

Lastly, a Personal Guarantee can be compared to a Florida Promissory Note. A Personal Guarantee is a promise made by an individual to repay a loan if the primary borrower defaults. Like a Promissory Note, it establishes a financial obligation. However, the key difference lies in the nature of the obligation. A Promissory Note is an agreement between the borrower and lender, while a Personal Guarantee involves a third party, providing additional assurance to the lender. This added layer can be particularly important in business loans or when the borrower has limited credit history.

When entering into a loan agreement in Florida, several documents often accompany the Promissory Note. These documents help clarify the terms of the loan and protect the interests of both the lender and the borrower. Below are four common forms that are typically used alongside the Florida Promissory Note.

These documents collectively enhance the clarity and security of the lending process. By ensuring that all parties are aware of their rights and responsibilities, they help facilitate a smoother transaction.