Attorney-Approved Florida Power of Attorney Document

Attorney-Approved Florida Power of Attorney Document

Understanding the Florida Power of Attorney (POA) form can be challenging, especially with the many misconceptions that exist. Here’s a list of ten common misunderstandings to help clarify the purpose and use of this important legal document.

Many people believe that a POA only handles financial decisions. In reality, a POA can also cover medical decisions, property management, and other personal matters, depending on how it is drafted.

Some think that once a POA is created, it remains in effect forever. However, a POA can be revoked or terminated at any time, as long as the principal is competent to make that decision.

While it is advisable to consult a lawyer, individuals can create a POA on their own using the appropriate forms, as long as they meet state requirements.

Many believe that a POA gives the agent absolute control over the principal's affairs. In fact, the powers granted can be limited to specific tasks or decisions, as outlined in the document.

Some people assume that only seniors need a POA. In truth, anyone can benefit from having a POA, especially those with health concerns or who travel frequently.

This confusion arises often. A POA allows someone to make decisions on your behalf, while a living will outlines your wishes regarding medical treatment in the event you cannot communicate them yourself.

While many choose family members as their agents, anyone can be designated, including friends or professionals, as long as they are trustworthy and willing to act in your best interest.

People often think a POA is only for when someone becomes incapacitated. However, it can also be useful for managing affairs during temporary absences, such as travel or hospitalization.

Many believe that a POA is set in stone. In fact, it can be modified or revoked at any time, provided the principal is competent to do so.

While a Florida POA is designed to comply with state laws, it may also be recognized in other states. However, it is essential to check local laws to ensure validity.

By addressing these misconceptions, individuals can make informed decisions about establishing a Power of Attorney that meets their needs and protects their interests.

After obtaining the Florida Power of Attorney form, the next step is to carefully fill it out to ensure it meets your needs and complies with state requirements. This process involves providing accurate information about yourself and the person you are designating as your agent. Follow the steps below to complete the form correctly.

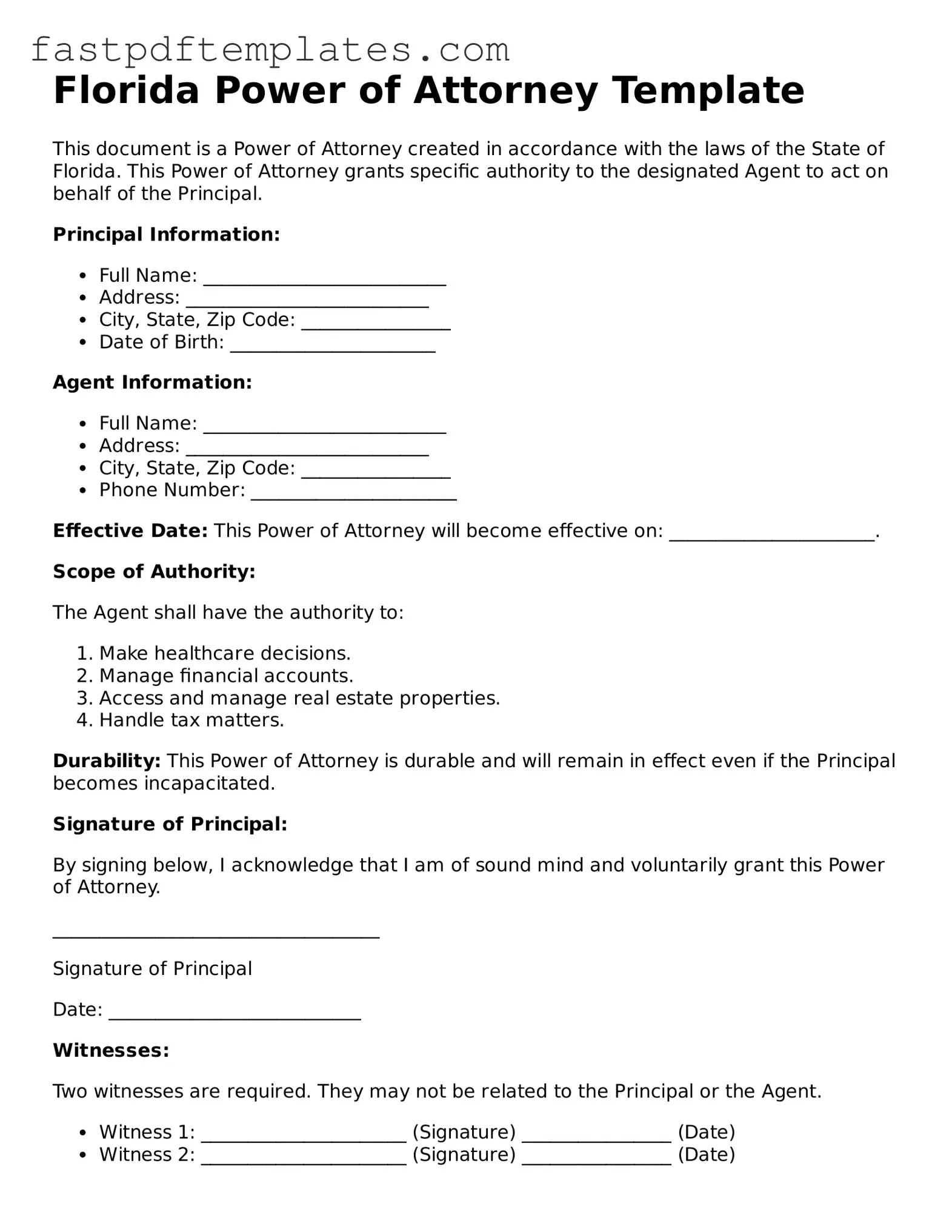

Florida Power of Attorney Template

This document is a Power of Attorney created in accordance with the laws of the State of Florida. This Power of Attorney grants specific authority to the designated Agent to act on behalf of the Principal.

Principal Information:

Agent Information:

Effective Date: This Power of Attorney will become effective on: ______________________.

Scope of Authority:

The Agent shall have the authority to:

Durability: This Power of Attorney is durable and will remain in effect even if the Principal becomes incapacitated.

Signature of Principal:

By signing below, I acknowledge that I am of sound mind and voluntarily grant this Power of Attorney.

___________________________________

Signature of Principal

Date: ___________________________

Witnesses:

Two witnesses are required. They may not be related to the Principal or the Agent.

Notary Public:

State of Florida

County of __________________________

Subscribed and sworn to before me this _____ day of ______________, 20__.

___________________________________

Notary Public Signature

My Commission Expires: ________________

Illinois Durable Power of Attorney Form - Can be effective immediately or upon a triggering event.

Poa Medical - Power of Attorney can be revoked at any time as long as you are mentally competent.

Free Michigan Power of Attorney Forms to Print - Your Power of Attorney can be paired with a living will for comprehensive planning.

Durable Power of Attorney Form California - A Power of Attorney can be limited to certain tasks or be comprehensive in nature.

When filling out the Florida Power of Attorney form, it's important to be careful and thorough. Here’s a list of things to do and not to do:

Taking these steps can help ensure that your Power of Attorney is valid and effective when you need it most.

Filling out and utilizing a Florida Power of Attorney (POA) form requires careful consideration. Here are six key takeaways to ensure proper understanding and execution:

By considering these key points, individuals can better navigate the process of creating and using a Power of Attorney in Florida.

The Florida Power of Attorney (POA) form is a legal document that allows one person to act on behalf of another in legal or financial matters. Similar to a POA, a Health Care Proxy grants someone the authority to make medical decisions for another individual when they are unable to do so. This document is particularly important in situations where a person is incapacitated and cannot communicate their wishes regarding medical treatment. The Health Care Proxy ensures that a trusted individual can advocate for the patient’s health care preferences, making it a vital tool for ensuring that one’s medical decisions align with their values and desires.

Another document that shares similarities with the Florida Power of Attorney is the Living Will. While a POA can cover a broad range of financial and legal matters, a Living Will specifically addresses end-of-life medical decisions. It allows individuals to express their wishes regarding life-sustaining treatments and interventions in situations where they may be terminally ill or in a persistent vegetative state. This document serves as a guide for healthcare providers and family members, ensuring that a person's preferences are honored during critical moments.

A Durable Power of Attorney is another closely related document. It functions similarly to a standard Power of Attorney but remains effective even if the principal becomes incapacitated. This durability is crucial for individuals who want to ensure that their financial and legal affairs are managed seamlessly, even if they can no longer make decisions themselves. By designating a trusted agent through a Durable Power of Attorney, individuals can maintain control over their affairs, providing peace of mind for themselves and their loved ones.

The Springing Power of Attorney is yet another variant. This document only becomes effective under specific conditions, typically when the principal becomes incapacitated. This type of POA can be particularly appealing for those who want to maintain control over their affairs while they are still capable of making decisions. It ensures that the appointed agent only steps in when truly necessary, providing a safeguard against potential misuse of authority.

A Trust is a legal arrangement that allows one person (the trustee) to hold assets for the benefit of another (the beneficiary). While a Power of Attorney allows someone to act on behalf of another in various matters, a Trust is specifically designed for asset management and distribution. Trusts can help avoid probate, provide tax benefits, and ensure that assets are managed according to the grantor's wishes. Both documents serve to protect individuals’ interests, but they do so in different ways.

A Guardianship is a legal relationship where a court appoints an individual to make decisions for someone who is unable to care for themselves. This can occur when a person is mentally incapacitated or a minor child needs a responsible adult to oversee their welfare. While a Power of Attorney allows individuals to designate their own agents, a Guardianship requires court intervention. Both serve to protect individuals, but the processes and levels of oversight differ significantly.

The Assignment of Benefits (AOB) is another document that can be compared to a Power of Attorney. An AOB allows a policyholder to transfer their insurance benefits to a third party, typically a contractor or service provider, to handle claims directly with the insurance company. This is common in home repair or medical services. Like a POA, it involves granting authority to another party, but it is specifically focused on insurance claims and benefits management.

Finally, a Financial Power of Attorney is a specific type of POA that focuses solely on financial matters. This document allows an agent to manage the principal's financial affairs, such as paying bills, managing investments, and filing taxes. While a general Power of Attorney can cover a wide array of decisions, a Financial Power of Attorney is tailored to address the complexities of financial management. This distinction is important for individuals who want to ensure that their finances are handled appropriately, especially during times of incapacity.

When creating a Florida Power of Attorney, it’s important to consider other documents that can complement this legal tool. Each of these forms serves a unique purpose and can help ensure that your wishes are respected and your affairs are managed effectively. Here are four common documents that often accompany a Power of Attorney.

Understanding these additional documents can help you create a comprehensive plan for your health and finances. Each form plays a vital role in ensuring that your wishes are honored and that your loved ones have the guidance they need during difficult times.