Attorney-Approved Florida Deed in Lieu of Foreclosure Document

Attorney-Approved Florida Deed in Lieu of Foreclosure Document

When facing financial difficulties, homeowners often explore various options to avoid foreclosure. One such option is a deed in lieu of foreclosure. However, several misconceptions surround this process. Understanding these can help homeowners make informed decisions.

By addressing these misconceptions, homeowners can better navigate their options and make choices that align with their financial goals.

After completing the Florida Deed in Lieu of Foreclosure form, the next steps involve submitting the document to the appropriate parties. This typically includes the lender and may require additional documentation to finalize the process. Ensure all parties involved are informed of the transfer and any implications it may have on the property.

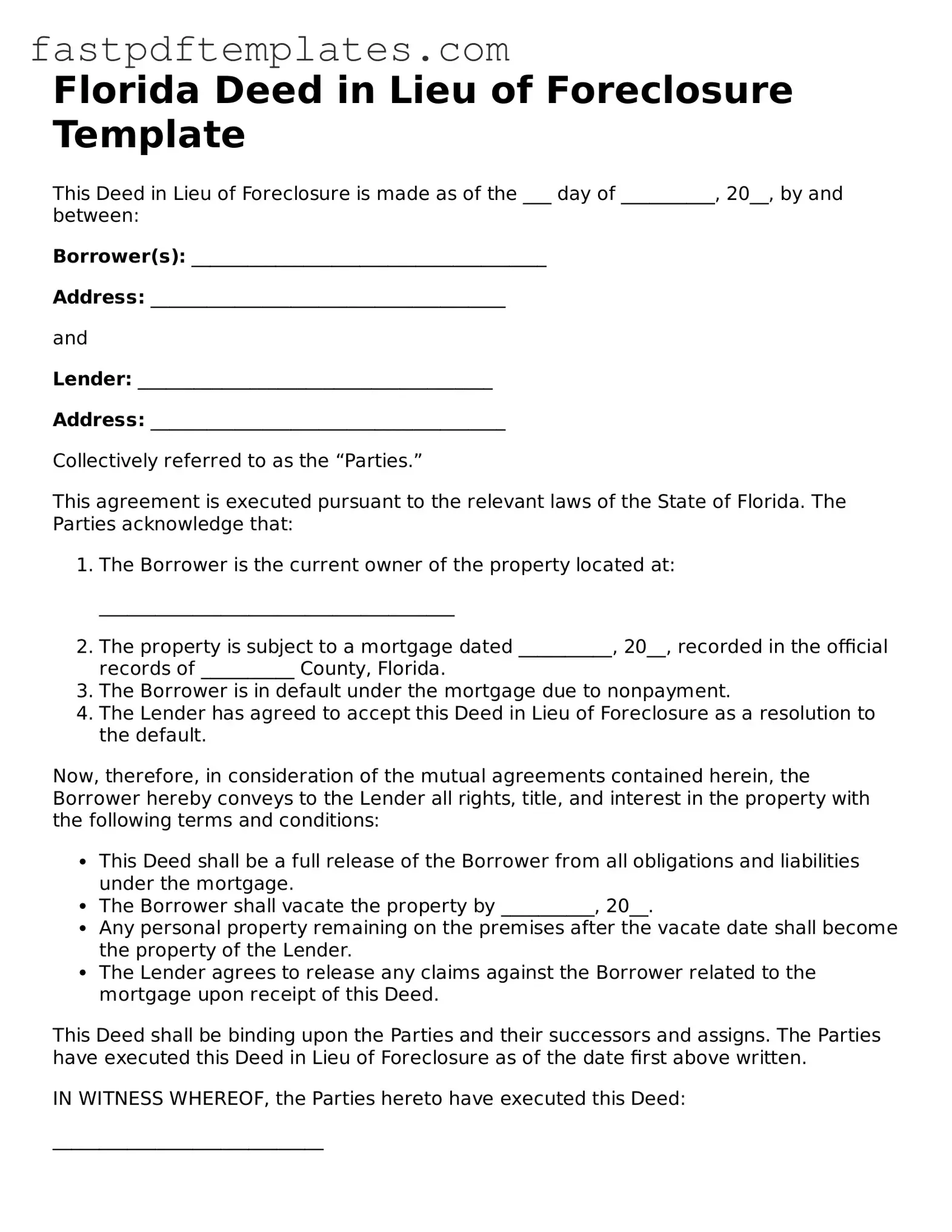

Florida Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is made as of the ___ day of __________, 20__, by and between:

Borrower(s): ______________________________________

Address: ______________________________________

and

Lender: ______________________________________

Address: ______________________________________

Collectively referred to as the “Parties.”

This agreement is executed pursuant to the relevant laws of the State of Florida. The Parties acknowledge that:

______________________________________

Now, therefore, in consideration of the mutual agreements contained herein, the Borrower hereby conveys to the Lender all rights, title, and interest in the property with the following terms and conditions:

This Deed shall be binding upon the Parties and their successors and assigns. The Parties have executed this Deed in Lieu of Foreclosure as of the date first above written.

IN WITNESS WHEREOF, the Parties hereto have executed this Deed:

_____________________________

Borrower Signature

Date: _______________________

_____________________________

Lender Signature

Date: _______________________

Deed in Lieu Vs Foreclosure - Homeowners might be able to negotiate a grace period after signing the deed for smoother transition.

Foreclosure Vs Deed in Lieu - This method can spare families from the emotional strain of foreclosure.

When filling out the Florida Deed in Lieu of Foreclosure form, it's important to follow certain guidelines to ensure the process goes smoothly. Here are some things you should and shouldn't do:

Filling out and using the Florida Deed in Lieu of Foreclosure form can be a significant step for homeowners facing financial difficulties. Here are some key takeaways to keep in mind:

By considering these takeaways, homeowners can navigate the complexities of the Deed in Lieu of Foreclosure process with greater confidence and clarity.

The Florida Deed in Lieu of Foreclosure is similar to a Mortgage Release form. Both documents serve to relieve the borrower of their obligations under the mortgage. In a Mortgage Release, the lender agrees to release the borrower from the mortgage debt, often after the property has been sold or transferred. This can help the borrower avoid a lengthy foreclosure process and the negative impact on their credit score that comes with it.

Another related document is the Short Sale Agreement. In a short sale, the lender agrees to accept less than the full amount owed on the mortgage when the property is sold. Like a Deed in Lieu of Foreclosure, this option allows the borrower to avoid foreclosure. However, a short sale involves selling the property to a third party, whereas a Deed in Lieu transfers ownership directly to the lender.

The Loan Modification Agreement is also similar. This document alters the terms of the existing mortgage, making it more manageable for the borrower. While a Deed in Lieu of Foreclosure involves giving up the property, a loan modification allows the borrower to keep their home while adjusting the payment terms to avoid default.

A Forebearance Agreement shares similarities as well. This document allows borrowers to temporarily pause or reduce their mortgage payments. While it does not result in a transfer of property like a Deed in Lieu, both options are designed to help borrowers manage financial difficulties and avoid foreclosure.

The Bankruptcy Filing can also be compared to a Deed in Lieu of Foreclosure. Both options can provide relief from overwhelming debt. Filing for bankruptcy can halt foreclosure proceedings, giving the borrower a chance to reorganize their debts. However, a Deed in Lieu directly transfers ownership of the property to the lender without the need for court intervention.

Another related document is the Property Settlement Agreement. This is often used in divorce proceedings where one spouse may transfer their interest in a property to the other. Similar to a Deed in Lieu, this agreement results in a change of ownership, but it is typically motivated by personal circumstances rather than financial distress.

The Quitclaim Deed is also noteworthy. This document allows a property owner to transfer their interest in the property to another party without guaranteeing that the title is clear. While a Deed in Lieu of Foreclosure is a formal arrangement with a lender to avoid foreclosure, a Quitclaim Deed can be used in various situations, including transferring property between family members.

The Assignment of Mortgage is another document that shares some similarities. This document allows a lender to transfer their interest in a mortgage to another party. While it does not involve the transfer of the property itself, it is part of the broader process of managing mortgage loans and can be used in conjunction with a Deed in Lieu of Foreclosure when the lender decides to sell the mortgage to another entity.

Finally, the Satisfaction of Mortgage is relevant. This document is issued by the lender once the mortgage has been fully paid off. It serves as proof that the borrower has fulfilled their obligations. In contrast, a Deed in Lieu of Foreclosure ends the mortgage by transferring the property back to the lender, but both documents ultimately signify the conclusion of the borrower's financial obligation to the lender.

When navigating the complex landscape of real estate transactions, especially in the context of foreclosure, several important documents often accompany the Florida Deed in Lieu of Foreclosure. Understanding these documents can help clarify the process and ensure all parties are well-informed. Here’s a brief overview of five key forms that are frequently used alongside the Deed in Lieu of Foreclosure.

Understanding these documents can empower homeowners facing foreclosure to make informed decisions. Each form plays a unique role in the process, and being aware of them can help facilitate a smoother transition during a challenging time.