Fillable Deed in Lieu of Foreclosure Document

Fillable Deed in Lieu of Foreclosure Document

When it comes to a Deed in Lieu of Foreclosure, many people have misconceptions that can lead to confusion. Let's clear up some of the most common misunderstandings.

Understanding these misconceptions can empower you to make informed decisions about your financial future. Always consult with a financial advisor or a legal expert when considering such options.

After completing the Deed in Lieu of Foreclosure form, you will need to submit it to your lender for review. They will assess the document and determine the next steps in the process. Be prepared for potential follow-up communication from the lender regarding any additional information or documentation they may require.

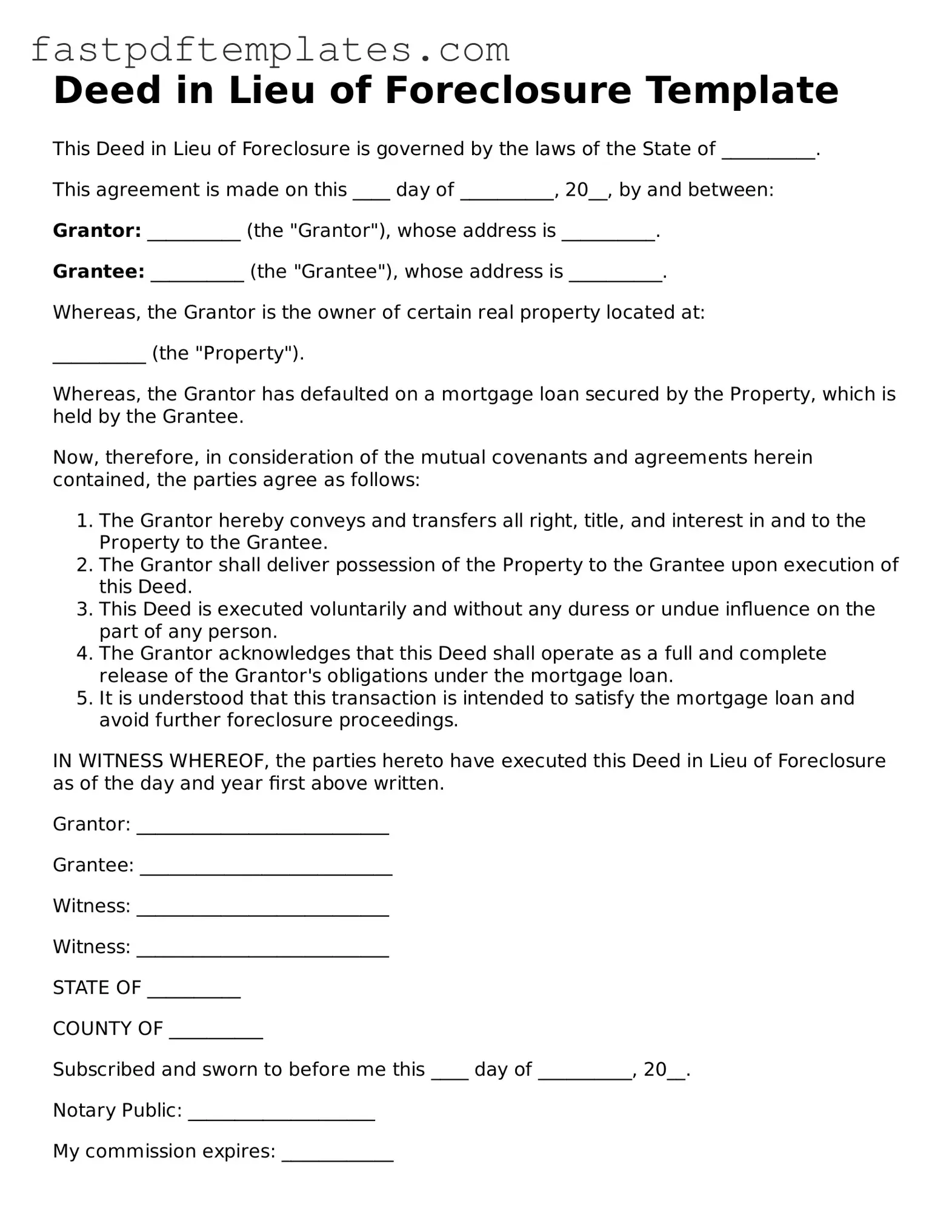

Deed in Lieu of Foreclosure Template

This Deed in Lieu of Foreclosure is governed by the laws of the State of __________.

This agreement is made on this ____ day of __________, 20__, by and between:

Grantor: __________ (the "Grantor"), whose address is __________.

Grantee: __________ (the "Grantee"), whose address is __________.

Whereas, the Grantor is the owner of certain real property located at:

__________ (the "Property").

Whereas, the Grantor has defaulted on a mortgage loan secured by the Property, which is held by the Grantee.

Now, therefore, in consideration of the mutual covenants and agreements herein contained, the parties agree as follows:

IN WITNESS WHEREOF, the parties hereto have executed this Deed in Lieu of Foreclosure as of the day and year first above written.

Grantor: ___________________________

Grantee: ___________________________

Witness: ___________________________

Witness: ___________________________

STATE OF __________

COUNTY OF __________

Subscribed and sworn to before me this ____ day of __________, 20__.

Notary Public: ____________________

My commission expires: ____________

Deed of Gift Property - Clearly stating intentions in the Gift Deed avoids disputes later on.

Does California Have a Transfer on Death Deed - Many people find this form to be a straightforward way to manage their real estate after they are gone.

Free Printable Michigan Lady Bird Deed Form - This deed reinforces the owner's control over the property, even after naming heirs.

When filling out a Deed in Lieu of Foreclosure form, it's important to approach the process carefully. Here are some key do's and don'ts to keep in mind:

By following these guidelines, you can help ensure a smoother process when completing your Deed in Lieu of Foreclosure form.

Filling out and using the Deed in Lieu of Foreclosure form requires careful consideration and understanding of the process. Here are ten key takeaways to keep in mind:

These key takeaways can help navigate the complexities of the Deed in Lieu of Foreclosure process, ensuring informed decisions are made.

A Deed in Lieu of Foreclosure is often compared to a short sale. In a short sale, the homeowner sells the property for less than the amount owed on the mortgage, with the lender's approval. This process allows the homeowner to avoid foreclosure while still relieving some of their debt. Both options provide a way for homeowners to exit their mortgage obligations, but a short sale typically requires a buyer, while a deed in lieu transfers the property directly to the lender.

Another similar document is the loan modification agreement. This agreement involves changing the terms of the existing mortgage to make it more manageable for the homeowner. The lender may lower the interest rate, extend the loan term, or even reduce the principal balance. Like a deed in lieu, a loan modification aims to help the homeowner avoid foreclosure, but it keeps the homeowner in the property rather than transferring ownership to the lender.

A foreclosure itself is a legal process where the lender takes possession of the property after the homeowner fails to make mortgage payments. While a deed in lieu is a voluntary agreement, foreclosure is often involuntary and can have severe consequences for the homeowner's credit. Both processes result in the homeowner losing their property, but a deed in lieu is generally considered a more amicable solution.

Bankruptcy is another option that can be similar to a deed in lieu of foreclosure. When a homeowner files for bankruptcy, they can reorganize their debts and potentially keep their home. In some cases, the bankruptcy process may lead to a deed in lieu if the homeowner decides that they can no longer maintain the property. Both bankruptcy and a deed in lieu can provide relief from overwhelming financial obligations, but they operate under different legal frameworks.

A property settlement agreement can also bear similarities to a deed in lieu. In situations where a couple is divorcing, they may agree to transfer property ownership to one spouse as part of the settlement. This transfer can relieve the other spouse of mortgage obligations. Like a deed in lieu, this agreement involves a voluntary transfer of property, but it is often tied to personal circumstances rather than financial distress.

Another related document is a quitclaim deed. This legal document allows one party to transfer their interest in a property to another without any warranties or guarantees. In situations where a homeowner is facing foreclosure, they might use a quitclaim deed to transfer their interest to a family member or friend. While this can sometimes help avoid foreclosure, it does not eliminate the mortgage obligation, unlike a deed in lieu.

Lastly, a mortgage release is a document that indicates a lender has agreed to release the borrower from their mortgage obligations. This can happen after a property is sold or when a lender agrees to forgive a portion of the debt. Similar to a deed in lieu, a mortgage release signifies that the borrower is no longer responsible for the mortgage, but it typically involves a sale or other transaction, rather than a direct transfer of the property back to the lender.

A Deed in Lieu of Foreclosure is an important document in the process of resolving a mortgage default. However, several other forms and documents are often used in conjunction with it. Each of these documents serves a specific purpose in ensuring a smooth transition and protecting the interests of both the borrower and the lender.

Understanding these documents is crucial for anyone navigating the Deed in Lieu of Foreclosure process. Each plays a role in protecting rights and ensuring a clear understanding of the transaction between the parties involved.