Blank Cg 20 10 07 04 Liability Endorsement Form

Blank Cg 20 10 07 04 Liability Endorsement Form

Misconceptions about the CG 20 10 07 04 Liability Endorsement form can lead to misunderstandings regarding coverage and obligations. Here are seven common misconceptions:

Understanding these misconceptions is essential for ensuring proper coverage and compliance with contractual obligations. Always review the specifics of the endorsement and consult with a professional if there are questions.

Filling out the CG 20 10 07 04 Liability Endorsement form is an important step in ensuring that the necessary parties are covered under your insurance policy. This form allows you to add additional insured parties to your commercial general liability coverage. Follow these steps to complete the form accurately.

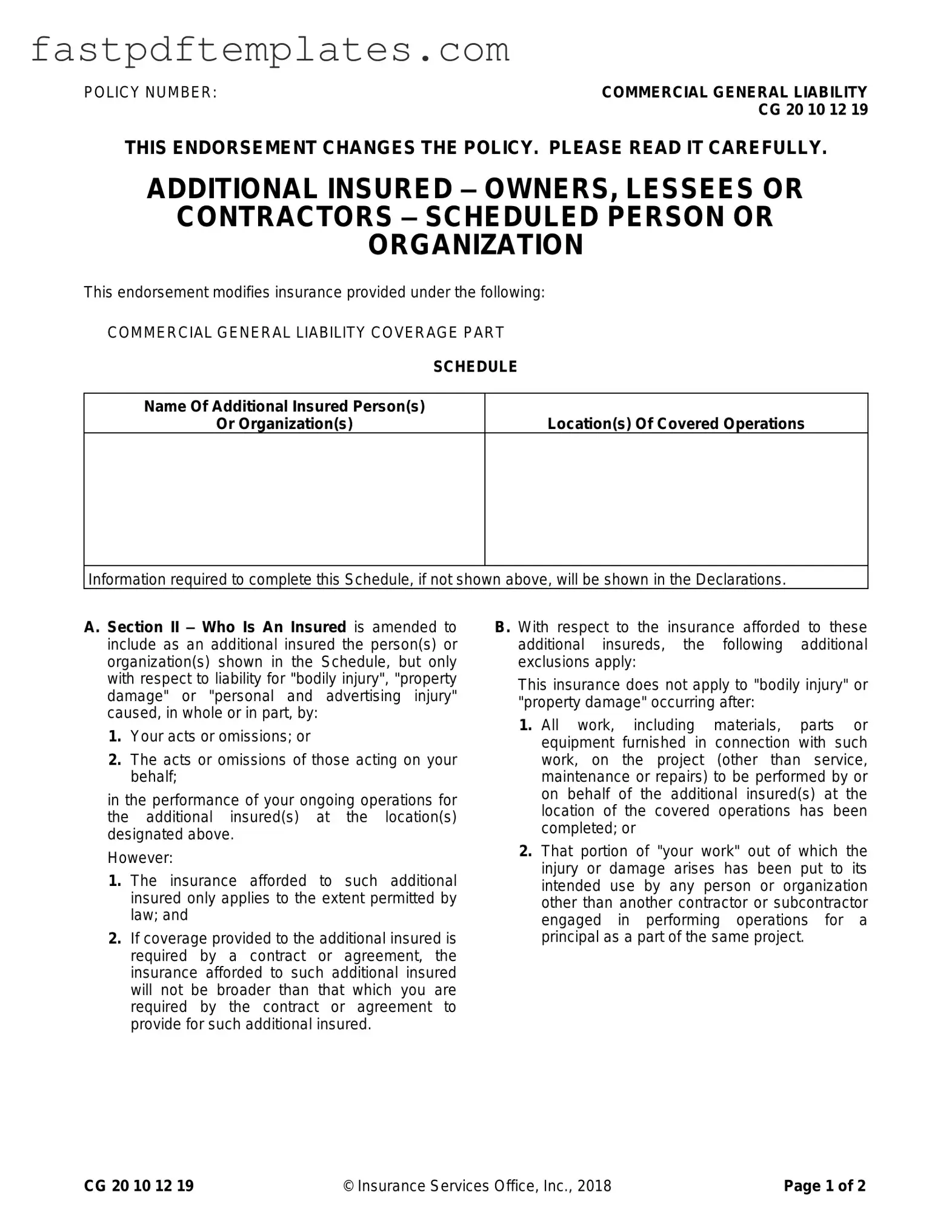

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

Broward Animal Care - The form is versatile for dogs, cats, ferrets, and other species.

Mvt 20-1 - Error-free completion of the form is critical for successful processing.

When filling out the CG 20 10 07 04 Liability Endorsement form, it’s essential to ensure accuracy and clarity. Here are five important dos and don’ts to keep in mind:

When filling out and using the CG 20 10 07 04 Liability Endorsement form, it’s essential to understand its implications and requirements. Here are some key takeaways:

The CG 20 10 07 04 Liability Endorsement form shares similarities with the CG 20 10 01 04 Additional Insured – Owners, Lessees, or Contractors form. Both documents serve to extend coverage to additional insured parties, typically required in construction contracts. They define the scope of coverage and specify the conditions under which the additional insured is protected against claims related to bodily injury or property damage. The key difference lies in the specific wording and limitations of coverage, as each endorsement may tailor the terms based on the needs of the primary insured and the contractual obligations involved.

Another related document is the CG 20 37 07 04 Additional Insured – Completed Operations form. This endorsement also adds additional insureds but focuses specifically on completed operations rather than ongoing operations. It provides coverage for claims arising from work that has been finished, which is crucial for contractors and subcontractors. This distinction is important as it addresses the timing of when coverage applies, helping to protect parties after a project is completed.

The CG 20 10 11 85 Additional Insured – Managers or Lessors of Premises endorsement is another similar document. It is designed to provide coverage to property managers and lessors, ensuring they are protected from claims arising from the use of their premises. Like the CG 20 10 07 04, it extends liability coverage but focuses on the specific context of property management. This endorsement emphasizes the importance of protecting those who may not be directly involved in the operations but have a vested interest in the property.

The CG 20 10 09 01 Additional Insured – Designated Person or Organization endorsement is similar in that it allows for the inclusion of specific individuals or organizations as additional insureds. This document is often used in contracts where specific parties need coverage, such as in joint ventures or partnerships. The key similarity lies in the intent to provide liability protection, but the application can vary based on the nature of the relationship between the parties involved.

The CG 20 10 10 01 Additional Insured – State or Governmental Agency endorsement also aligns with the CG 20 10 07 04 form. This endorsement is tailored for situations where state or governmental entities require additional insured status. It ensures that these entities are protected from claims arising out of the operations of the primary insured. The similarity lies in the extension of coverage, but the specific requirements and limitations can differ based on governmental regulations.

The CG 20 10 13 04 Additional Insured – Grantor of Franchise endorsement further exemplifies the concept of extending coverage to additional insureds. This document is specific to franchise agreements, providing liability protection to the franchisor. The endorsement shares the fundamental purpose of extending coverage but is tailored to address the unique risks associated with franchise relationships, highlighting the importance of context in liability insurance.

Lastly, the CG 20 10 08 01 Additional Insured – Vendors endorsement is relevant as it extends coverage to vendors of the primary insured. This form ensures that vendors are protected against claims arising from the products or services they provide. The similarity with the CG 20 10 07 04 lies in the overarching goal of providing liability protection, but the focus on vendor relationships introduces different considerations regarding risk management and liability exposure.

The CG 20 10 07 04 Liability Endorsement form is an important document in the realm of commercial general liability insurance. It provides coverage for additional insured parties, such as owners, lessees, or contractors. However, this form is often used alongside other documents that help clarify coverage and responsibilities. Below is a list of related forms and documents that may be relevant.

Understanding these documents can help ensure that all parties involved are adequately protected and aware of their responsibilities. Always consult with a qualified professional when dealing with insurance matters to ensure compliance and clarity.