Attorney-Approved California Promissory Note Document

Attorney-Approved California Promissory Note Document

When it comes to the California Promissory Note form, there are several misconceptions that can lead to confusion. Here are ten common misunderstandings:

Understanding these misconceptions can help individuals navigate the world of promissory notes more effectively. It's essential to approach these documents with clarity and awareness to ensure all parties are protected.

Once you have the California Promissory Note form in front of you, it's time to fill it out. Make sure you have all necessary information ready, such as the details of the borrower, lender, and the terms of the loan. Follow these steps to complete the form accurately.

After completing the form, review it for any errors or missing information. Once everything is accurate, make copies for both parties. Keep the original in a safe place.

California Promissory Note Template

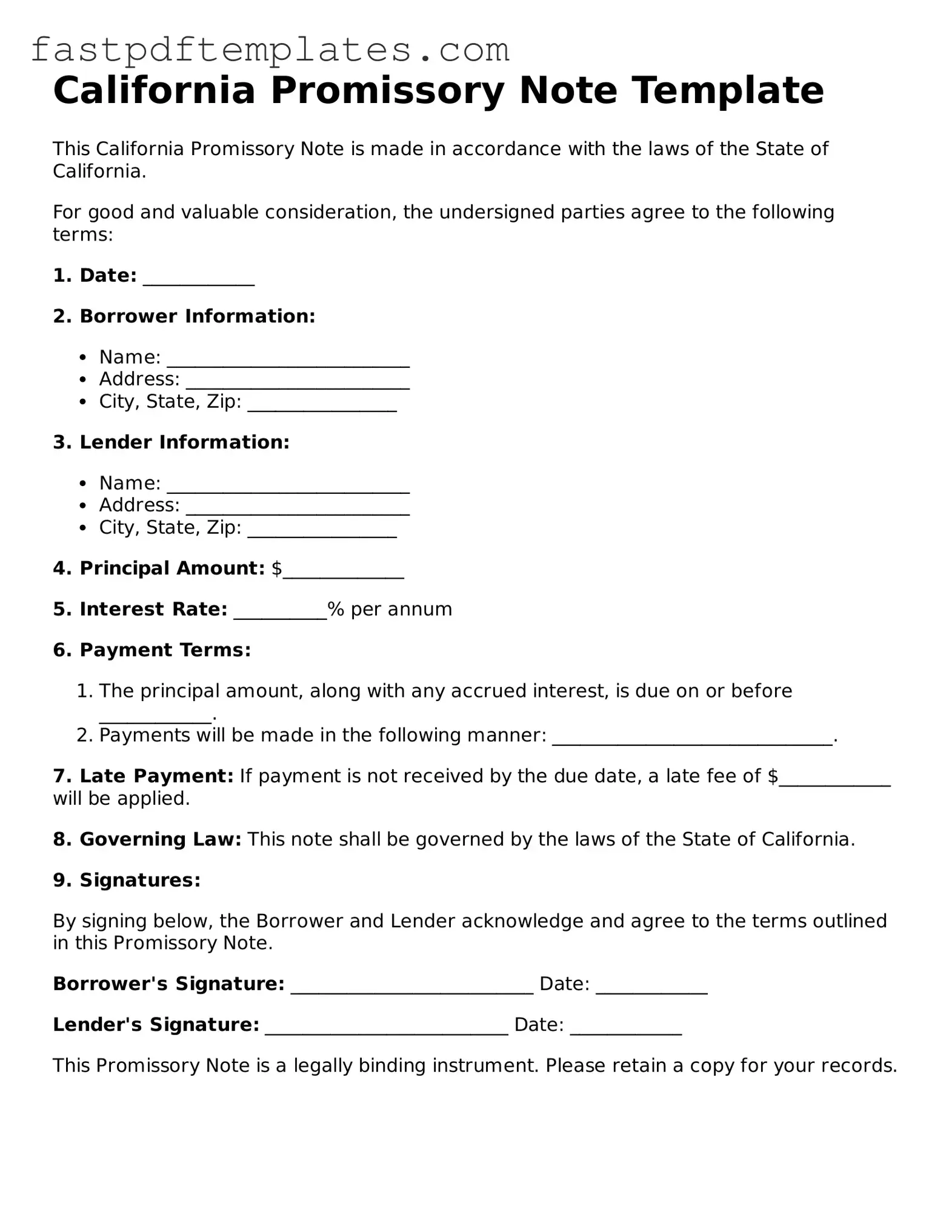

This California Promissory Note is made in accordance with the laws of the State of California.

For good and valuable consideration, the undersigned parties agree to the following terms:

1. Date: ____________

2. Borrower Information:

3. Lender Information:

4. Principal Amount: $_____________

5. Interest Rate: __________% per annum

6. Payment Terms:

7. Late Payment: If payment is not received by the due date, a late fee of $____________ will be applied.

8. Governing Law: This note shall be governed by the laws of the State of California.

9. Signatures:

By signing below, the Borrower and Lender acknowledge and agree to the terms outlined in this Promissory Note.

Borrower's Signature: __________________________ Date: ____________

Lender's Signature: __________________________ Date: ____________

This Promissory Note is a legally binding instrument. Please retain a copy for your records.

Texas Promissory Note - This document serves as evidence of a loan and outlines the borrower's obligations.

Illinois Promissory Note - The promissory note can specify whether the payment is due in installments or as a lump sum.

Promissory Note New York - A promissory note is a written promise to pay a certain amount of money to someone.

When filling out the California Promissory Note form, it is essential to follow certain guidelines to ensure clarity and legality. Here is a list of things you should and shouldn't do:

When filling out and using the California Promissory Note form, keep these key takeaways in mind:

By paying attention to these key points, you can create a clear and effective promissory note that protects both parties involved.

A personal loan agreement shares similarities with the California Promissory Note. Both documents outline the terms of a loan, including the amount borrowed, the interest rate, and the repayment schedule. The personal loan agreement may also include additional clauses related to late fees or default conditions. Like the promissory note, it serves as a legal commitment by the borrower to repay the loan under specified terms. Both documents are crucial in establishing a clear understanding between the lender and borrower regarding their financial obligations.

A mortgage agreement is another document akin to the California Promissory Note. While a mortgage specifically secures a loan with real property, it often includes a promissory note as part of the transaction. The note details the borrower's promise to repay the loan, while the mortgage agreement outlines the rights of the lender in case of default. Both documents work together to ensure that the lender has recourse to recover the loan amount, making them integral to real estate financing.

A car loan agreement also resembles the California Promissory Note. This document specifies the terms under which a borrower agrees to repay a loan used to purchase a vehicle. Similar to a promissory note, it includes details such as the loan amount, interest rate, and repayment schedule. The car loan agreement typically grants the lender a security interest in the vehicle, ensuring that they can reclaim it if the borrower defaults. Both documents create a legal framework for the transaction, protecting the interests of both parties.

A business loan agreement is comparable to the California Promissory Note as well. This document outlines the terms of a loan provided to a business entity. It includes the loan amount, interest rate, repayment schedule, and any collateral involved. Like a promissory note, it serves as a binding agreement, ensuring that the business commits to repaying the loan. Both documents are essential in establishing the lender's rights and the borrower's responsibilities in a business financing context.

Finally, an installment agreement can be viewed as similar to the California Promissory Note. This document outlines the terms under which a borrower agrees to repay a debt in installments over a specified period. It typically includes the total amount owed, the payment schedule, and any applicable interest rates. Like a promissory note, it is a legally binding contract that ensures the borrower understands their obligation to make regular payments. Both documents aim to clarify the repayment terms and protect the interests of the lender.

When using a California Promissory Note, several other forms and documents may be helpful to ensure clarity and protect the interests of all parties involved. Below are some commonly used documents that accompany a Promissory Note.

Using these documents alongside a California Promissory Note can help clarify expectations and responsibilities, making the borrowing process smoother for everyone involved.