Blank Business Credit Application Form

Blank Business Credit Application Form

Understanding the Business Credit Application form is crucial for any business seeking credit. However, several misconceptions can lead to confusion and potential issues. Here are nine common misconceptions:

Many believe that submitting a Business Credit Application guarantees approval. In reality, lenders assess various factors, including credit history and financial stability, before granting credit.

Some think that only big corporations require a Business Credit Application. However, small businesses and startups also need to complete this form to access credit options.

Many applicants assume that their personal credit history does not affect their business credit application. In fact, lenders often review personal credit scores, especially for small businesses without established credit histories.

Some view the application as a mere formality. In truth, it is a critical document that provides lenders with essential information to make informed decisions.

There is a misconception that minor inaccuracies won't matter. However, providing false or misleading information can lead to denial of credit or even legal repercussions.

Many believe that the application is set in stone once submitted. In reality, applicants can often update or correct information if they realize there are errors.

Some think that Business Credit Applications are only necessary for loans. In fact, they are also essential for obtaining lines of credit, credit cards, and vendor accounts.

Many assume that all lenders evaluate applications in the same way. However, each lender has unique criteria and processes, which can significantly affect approval outcomes.

Some believe that the credit limit assigned upon approval remains unchanged. In reality, credit limits can be reviewed and adjusted based on the business’s financial performance and credit behavior.

By dispelling these misconceptions, businesses can better navigate the credit application process and make informed decisions about their financial future.

Once you have the Business Credit Application form ready, you will need to complete it accurately. This will help ensure a smooth review process for your application. Follow these steps to fill out the form correctly.

After completing the form, review all the information for accuracy. Once everything is in order, submit the application according to the provided instructions. You will receive further communication regarding the status of your application.

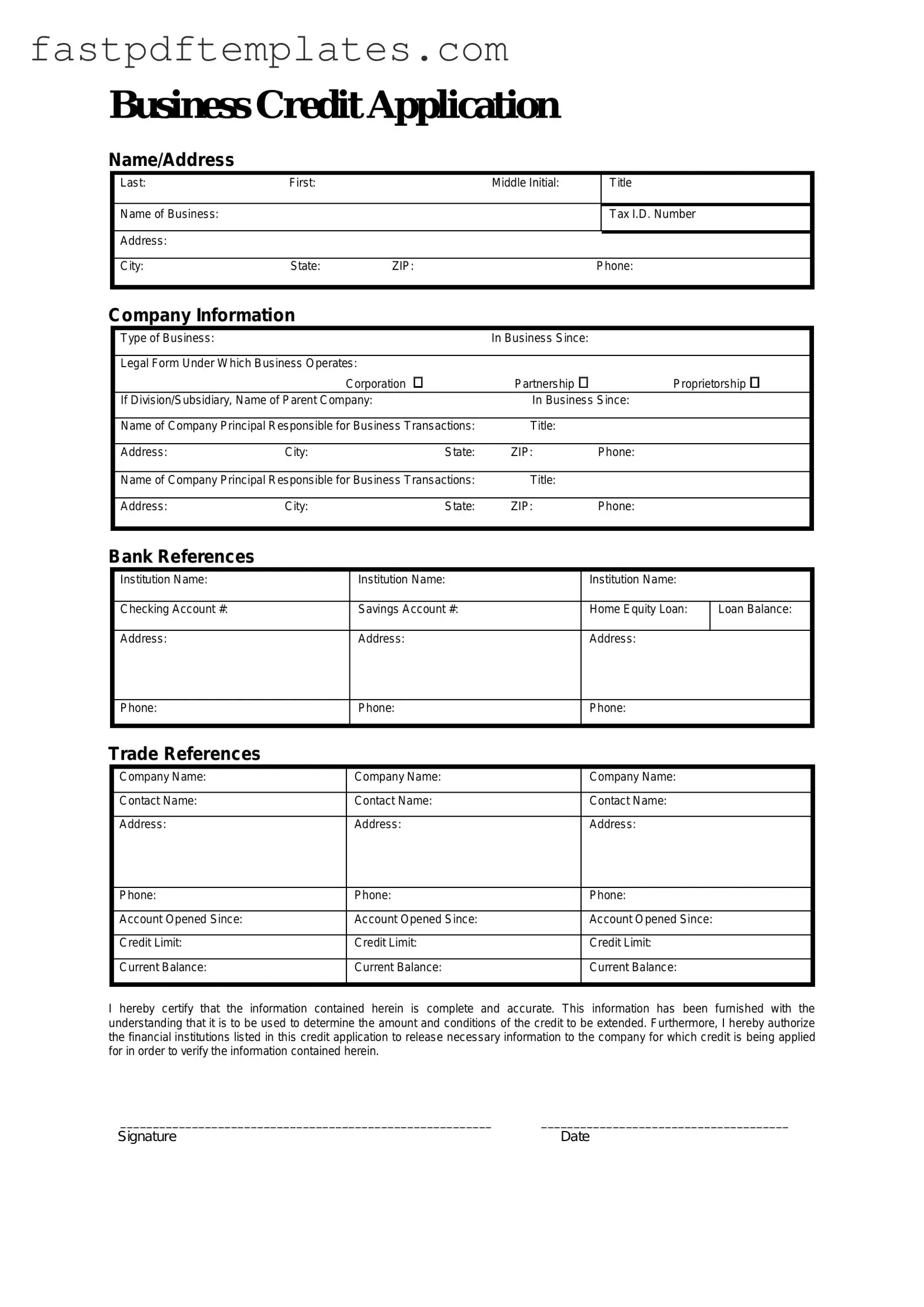

Business Credit Application

Name/Address

Last: |

First: |

|

Middle Initial: |

|

Title |

|

|

|

|

|

|

Name of Business: |

|

|

|

|

Tax I.D. Number |

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

|

City: |

State: |

ZIP: |

|

Phone: |

|

|

|

|

|

|

|

Company Information

|

Type of Business: |

|

|

|

In Business Since: |

|

|

|

|

|

|

|

|

|

|

||

|

Legal Form Under Which Business Operates: |

|

|

|

|

|||

|

|

|

Corporation |

Partnership |

Proprietorship |

|

||

|

If Division/Subsidiary, Name of Parent Company: |

In Business Since: |

|

|||||

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

|

|

Bank References |

|

|

|

|

|

|

|

|

|

Institution Name: |

|

|

Institution Name: |

|

Institution Name: |

||

|

|

|

|

|

|

|

|

|

|

Checking Account #: |

|

|

Savings Account #: |

|

Home Equity Loan: |

ILoan Balance: |

|

|

Address: |

|

|

Address: |

|

Address: |

|

|

Phone:

Phone:

Phone:

Trade References

Company Name: |

Company Name: |

Company Name: |

|

|

|

Contact Name: |

Contact Name: |

Contact Name: |

|

|

|

Address: |

Address: |

Address: |

|

|

|

Phone: |

Phone: |

Phone: |

|

|

|

Account Opened Since: |

Account Opened Since: |

Account Opened Since: |

|

|

|

Credit Limit: |

Credit Limit: |

Credit Limit: |

|

|

|

Current Balance: |

Current Balance: |

Current Balance: |

|

|

|

I hereby certify that the information contained herein is complete and accurate. This information has been furnished with the understanding that it is to be used to determine the amount and conditions of the credit to be extended. Furthermore, I hereby authorize the financial institutions listed in this credit application to release necessary information to the company for which credit is being applied for in order to verify the information contained herein.

_________________________________________________________ ______________________________________

Signature |

Date |

Employee Change Form Template - Notify about part-time employees transitioning to full-time status.

Parent Consent Letter for Travel - This consent form requires parental signatures to validate travel plans for children.

How to Create Pay Stubs for Self Employment - Helps establish a professional payment record for contractors.

When filling out a Business Credit Application form, it is important to follow certain guidelines to ensure accuracy and completeness. Here are six things to do and not do:

Filling out and using a Business Credit Application form is crucial for establishing a business's creditworthiness. Here are key takeaways to consider:

The Business Credit Application form is similar to a Loan Application form. Both documents serve to assess the financial stability and creditworthiness of an applicant. A Loan Application typically requires detailed information about the borrower's income, debts, and assets. Similarly, the Business Credit Application seeks to gather comprehensive data about a business's financial health, including revenue, expenses, and existing credit lines. This information helps lenders make informed decisions regarding the extension of credit.

Another document akin to the Business Credit Application is the Vendor Credit Application. Vendors often require businesses to complete this form before extending credit for goods or services. Like the Business Credit Application, it collects essential information about the business's financial history and payment practices. Both documents aim to mitigate risk for the creditor by ensuring that the applicant can meet their financial obligations.

The Personal Financial Statement shares similarities with the Business Credit Application as well. This document provides a snapshot of an individual's financial situation, including assets, liabilities, and net worth. When a business owner submits a Business Credit Application, personal financial information may also be required to assess the owner's ability to guarantee the business's debts. Thus, both documents focus on financial transparency and accountability.

The Business Loan Agreement is another related document. Once a credit application is approved, the terms of the loan are outlined in this agreement. While the Business Credit Application assesses eligibility, the Loan Agreement details the obligations and rights of both parties. It includes information such as loan amounts, interest rates, and repayment schedules, all of which stem from the initial application process.

The Credit Reference Request form is also comparable. This document is used to gather information from other creditors about the applicant's payment history and credit behavior. Similar to the Business Credit Application, it aims to evaluate the risk involved in extending credit. Both documents rely on external validation to support the decision-making process regarding creditworthiness.

The Financial Statement is yet another document that mirrors the Business Credit Application. It provides a detailed account of a company's financial performance over a specific period. Lenders often require this statement to assess the business's profitability and cash flow. Both documents are crucial in evaluating whether a business can sustain additional credit without jeopardizing its financial stability.

Lastly, the Partnership Agreement can be seen as similar in nature. This document outlines the terms and conditions under which business partners operate. When a business applies for credit, lenders may review the Partnership Agreement to understand the roles and responsibilities of each partner. This understanding is vital, as it impacts the business's ability to repay any credit extended, just as the Business Credit Application does.

When applying for business credit, several forms and documents may accompany the Business Credit Application form. These documents provide additional information and help establish the creditworthiness of the business. Below is a list of commonly used forms and their brief descriptions.

Having these documents ready can streamline the credit application process and improve the chances of approval. Each document plays a vital role in presenting a complete picture of the business's financial standing and reliability to potential lenders.